Welcome to the July 2025 Newsletter. This month, we’re discussing the economy, employment, financial terminology, and more.

Summary

On June 12, Josh Brown, CEO of Ritholtz Wealth Management in New York City, said on CNBC, “I think we are stuck in this paradigm of the ‘Fed feels it should not act’, as we have softness in the labor market, and we are seeing a real deceleration in the economy except for AI spend. There continues to be a lot happening with tariffs and the tax bill. The big story during the second half of the year will be the US economy and corporate profits.”

Quote of the Day

Dave Ramsey said on his radio show during the week of June 9, “The fastest way to get rich is to get rich slowly.”

At Lorenz Financial, we believe Dave is saying:

- Always spend less than you make.

- Permanently get out of debt.

- Use an online budget tool to plan all monthly spending and then track what was actually spent. Then analyze where excess spending occurred and correct it during the next month. Repeat every month.

- Other than borrowing for a fixed-rate, first mortgage on your primary home with a monthly payment of principal + interest + insurance + real estate taxes less than 25% of family take-home pay, never borrow money again.

- Don’t spend excessively on cars, trucks, boats, snowmobiles, jet skis, etc. The value of all assets with an engine or motor should not exceed 50% of the family annual income.

- Don’t let an emergency wipe you out by having an emergency fund less than 3 to 6 months of family spending.

- Save 15% of your family’s gross monthly income for retirement by investing in the stock market or income-producing real estate.

Pop Quiz

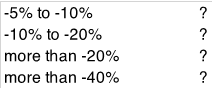

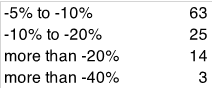

Since World War II (80 years ago), how many times has the S&P 500 Index dropped by the following percentages from a recent high?

The answer to this month’s Pop Quiz is at the bottom of the newsletter.

The Economy

Employment

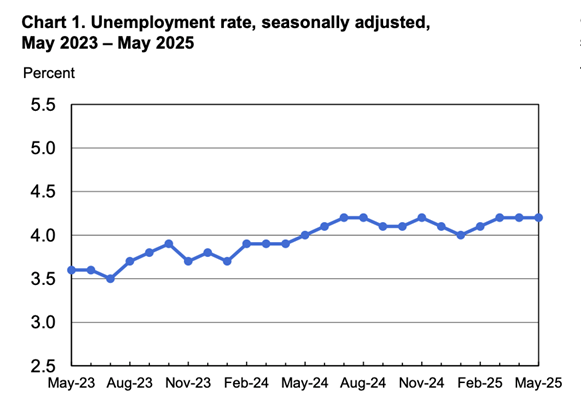

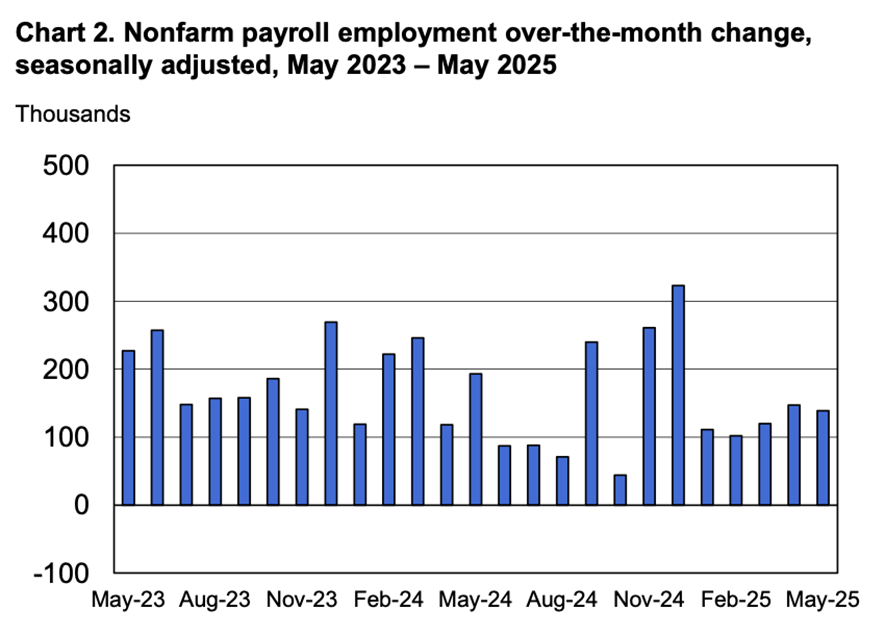

Total U.S. nonfarm payroll employment rose by 139,000 in May. The official unemployment rate, U-3, remained the same at 4.2%. The March and April 2025 combined employment numbers were revised lower by 95,000 than previously reported.

Chart 1 below is based on the Bureau of Labor Statistics official unemployment rate, U-3.

Chart 2 below shows the two-year trend of employment growth.

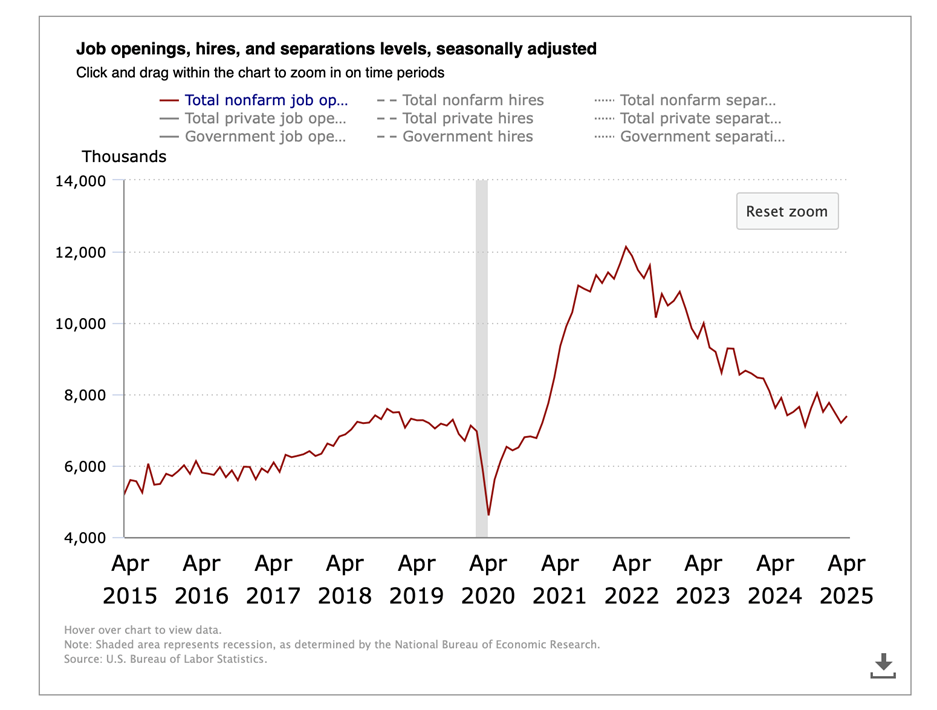

The Job Openings & Labor Turnover Survey (JOLTS) increased slightly to 7.4 million open jobs across the country as of the last business day in April. It was 7.2 million in the prior month. The 10-year chart below shows that the downward trend continues in open jobs since March 2022.

The seasonally adjusted Total U.S. Unemployment Rate, U-6, remained the same at 7.8% in May as compared to the prior month. There were 6.8 million people unemployed in May, age 16 and older. Last month it was 6.6 million people unemployed.

May Unemployment Rates by Education Level

Average hourly earnings of all employees on private nonfarm payrolls were up 3.9% in May compared to a year ago. It was 3.8% the previous month.

| Less Than High School Diploma | 5.5% |

| High School Graduate, No College | 4.5% |

| Some College, Associate's Degree, or Skilled Trade Degree | 3.3% |

| Bachelor's Degree or Higher | 2.6% |

Leading Economic Indicators (LEI) sponsored by The Conference Board

The LEI decreased only 0.1% in May. The Conference Board’s spokesperson said, “Consumer pessimism, persistently weak new orders in manufacturing, a second consecutive month of rising initial unemployment claims, and a decline in housing permits weighed on the LEI Index. The Conference Board does not anticipate a recession, but we do expect a significant slowdown in economic growth in 2025 compared to 2024. We expect real GDP growth of 1.6% this year.”

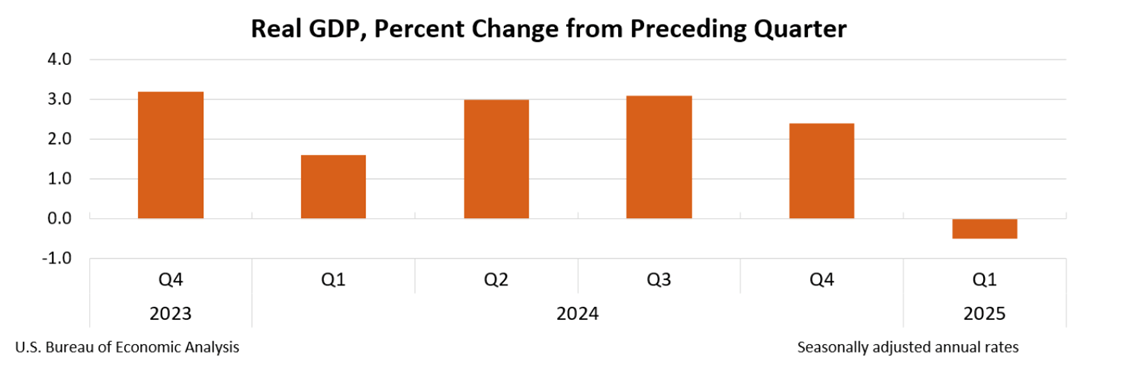

Gross Domestic Product (GDP)

The Bureau of Economic Analysis said the third estimate for GDP in the first quarter of 2025 decreased at an annual real rate of 0.5%. GDP for the fourth quarter of 2024 was +2.4%.

The decrease in the first quarter GDP reflected a substantial increase in imports, which are a subtraction in the GDP calculation. For the year 2024, GDP increased 2.8% and grew 3.2% in 2003.

Labor Productivity – Quarterly

Annualized and seasonally adjusted, nonfarm, business-sector labor productivity was a disappointment decreasing by a revised 1.5% in the first quarter of 2025 as reported by the Bureau of Labor Statistics. The original report had labor productivity decreasing only 0.8%. For the same quarter a year ago, labor productivity increased 1.4%.

By calendar year, labor productivity grew a revised 2.8% in 2024 and 1.9% in 2023.

Inflation – No change since last month at the time of this newsletter publication.

Annual inflation decreased to 2.1% as measured by the Personal Consumption Expenditures (PCE) price index for April. The revised annual March number was 2.3% during the prior 12 months. The core PCE price index, which excludes food and energy, decreased to 2.5% in April. It was 2.6% in March and 3.0% in February.

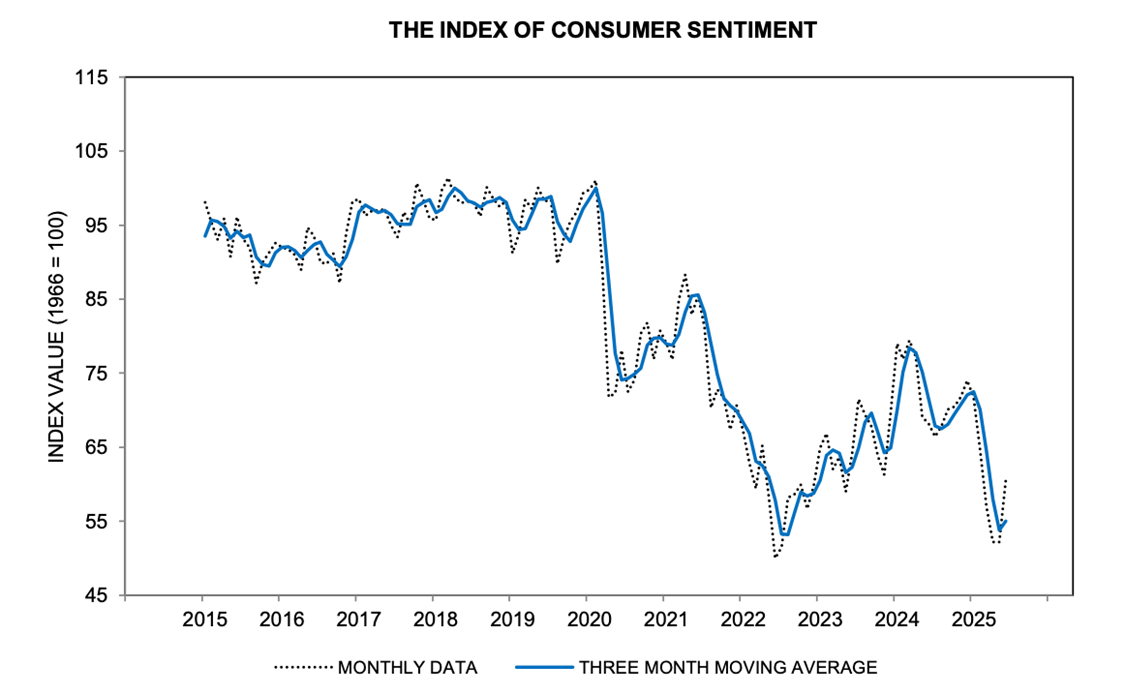

University of Michigan Consumer Sentiment

Consumer sentiment in June rose to 60.5 compared to May’s 52.2. The increase was the first in six months. See the 10-year chart below.

All five index components rose in May, but consumers still perceive wide-ranging downside risks to the economy. Despite this month’s notable improvement, consumers remain guarded and concerned about the trajectory of the economy.

Mortgage Rates and Average Existing Home Prices

As of June 25, 2025, the average 30-year fixed-rate mortgage had an interest rate of 6.82%, compared to 6.97% last month. The average 15-year fixed-rate mortgage had an interest rate of 6.04%, compared to 6.23% last month.

The median existing-home sale price increased in May 2025 to $422,800 from $417,200 in May 2024. The volume of existing home sales decreased 0.7% compared to a year earlier, according to the National Association of Realtors. The inventory of existing homes for sale dramatically increased by 6.2% to a 4.6-month supply in May. The desired supply target is 6 months.

The U.S. Public Debt as Issued by the Treasury Department as of June 25, 2025, was:

$37,030,000,000,000.

Last month it was $36,914,000,000,000.

Important Dates in July

THE STOCK MARKET

Commentary

This month we have comments from Brad Gerstner, CEO of the hedge fund, Altimeter Capital. Gerstner was asked, “Please give us the lay of the land as you see it.”

Gerstner said, “First, I feel very comfortable where we are going to land the plane on tariffs. Second, it looks increasing likely the reconciliation bill will get signed into law. These two items will add certainty to the markets and add stimulus to the economy.”

“The third thing that is coming is interest rate cuts by the Federal Reserve in the back half of the year. That is an effective trifecta for the economy. Behind all of this is the Artificial Intelligence Supercycle. So long as these thangs happen, the economy is ready to cook” (in a good way.)

Stock Market Valuation

Hank Smith of Haverford Trust said on June 17 on CNBC, “The stock market is near an all-time high in anticipation of certainty replacing uncertainty on tariffs, the 2017 tax cuts getting extended, deregulation quickening, AI productivity increasing in corporations and government, and the Federal Reserve easing short-term interest rates. If this occurs, the economy and the stock market should accelerate in the 2nd half of 2025 and into 2026.”

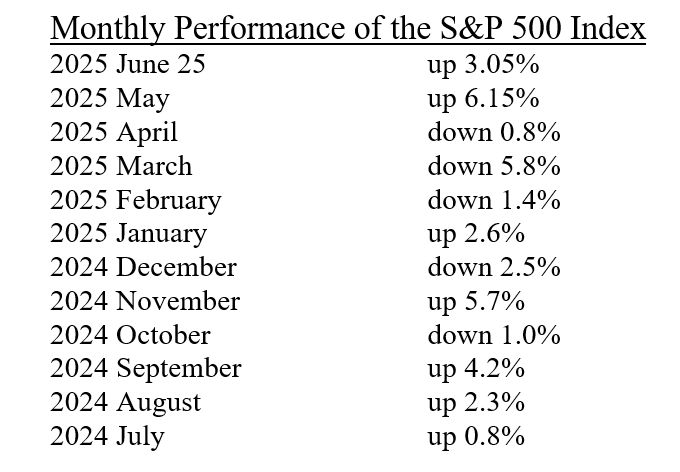

The S&P 500 Index closed on June 25, 2025 at 6,092.16. Year to date the market is up 3.6%.

Prior Annual S&P 500 Performance As Per The Exchange Traded Fund, VOO

2024: +24.98%

2023: +26.32%

2022: -18.19%

2021: +28.78%

2020: +18.29%

2019: +31.35%

Recommended Action for Your Stock Portfolio

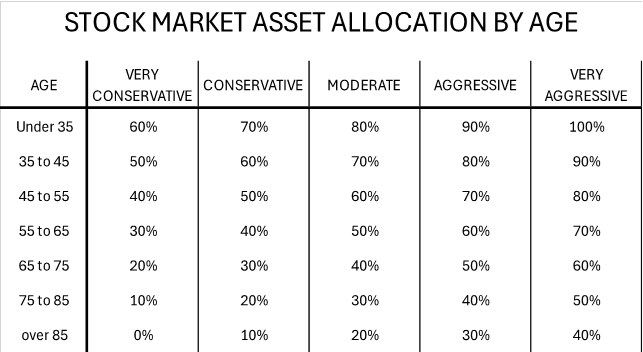

What is your risk tolerance? This is the most challenging question for every investor!

One factor is our age. The older we get, the more conservative we likely become. Another factor is an investor’s needs and objectives. For example, Warren Buffett could easily say, “I have enough money”, and conclude that all he needs are Treasury Bonds and no more stocks. But that would go against his nature. Even at 94, Buffett is 100% in the stock market except for his cash in short-term Treasury bills which is available to buy more stock when he finds a good deal.

Below is a chart that represents A STARTING POINT to help investors determine THEIR risk tolerance. This chart only considers age, so this is not an investor’s endpoint, but only a starting point to determine their risk tolerance. The greater the risk tolerance of the investor, the greater the percentage of their portfolio should be in the stock market. The numbers below represent the percentage a portfolio should be in the stock market as per the five basic styles of investing.

An investor is not limited to only being in one column during their lifetime. A stressful medical situation at age 50 could throw a family from the aggressive column to the conservative column. Don’t dismiss the need to talk to a professional financial advisor to help you figure out your risk tolerance. And don’t be so casual about this by saying, “Well, I guess I am moderate”.

An important consideration for long-term sustainability, a portfolio must stay ahead of inflation and taxes. Therefore, a portfolio needs to be at least 35% to 40% in the stock market on a long-term basis – just to stay even!

• Not FDIC Insured • No Bank Guarantee • May Lose Value

Financial Markets Vocabulary

What is your FICO Score based on? It is based on the following:

- Payment History: 35%

- Amount Owed: 30%

- Length of Credit: 15%

- Credit Mix: 10%

- New Credit: 10%

TOTAL 100%

Payment History – This is the single most important factor in determining a FICO score. It reflects how consistently you pay your debts on time. A consistent payment history with on-time payments is crucial for a good credit score. Late payments, even by one day, will negatively impact your score. The more past due items you have, the lower your score will be. The longer an account is past due, the more it will hurt your score.

For example, you have made payments on time for months, but in June, money was very tight, and you skipped a credit card payment. Later, you were able to make your payment on time in July, August, and beyond. Is this a big problem? Yes, as your payment in July was actually your June payment that was 30 days late. Your payment in August was actually your July payment, which was another 30 days late. This is very bad! This pattern will go on forever until you catch up on your payments. Please never skip a payment or have a late payment!

Amount Owed – This refers to the total debt you carry across all your credit accounts. Credit utilization is calculated by dividing your total outstanding balance by your total available credit limits. A lower credit utilization rate (meaning you’re using a smaller percentage of your available credit) generally results in a higher score. The number of accounts with outstanding balances is also considered, with fewer accounts with balances generally being better. Please try to maintain a maximum credit utilization of 20% to 25% to maximize your FICO score.

A change coming almost immediately is the inclusion of “Buy Now, Pay Later” (BNPL) loans in a borrower’s total debt calculation. Nationwide, this debt was $94 billion in 2024 and is expected to grow 15% in 2025. The inclusion of this debt will very likely lower everyone’s FICO score who uses BNPL loans. Our recommendation is to never use these types of loans.

Next month, we will review the length of credit, credit mix, and new credit in determining your FICO score. Yes, we are different than Dave Ramsey in this regard. We believe everyone should strive to maximize their FICO score.

OK, Now What Do I Do?

Financial Questions for Engaged Couples

This month, we continue with our third of a four-month-long series of appropriate financial questions for engaged couples. Assuming an engaged couple is not receiving financial counseling prior to getting married from another source, below are our suggested questions. Parents and grandparents, please get involved.

INVESTMENTS AND RETIREMENT

1. What is your risk tolerance or tolerance for the volatility of your future investments?

2. How much money will you need to retire?

3. How do you plan to create significant wealth over your lifetime?

4. Regarding your investments, do you think you are a long-term investor who exhibits patience and courage, or are you a short-term trader?

5. Today, how is each spouse saving for retirement? How does each spouse have their retirement money invested today?

6. Under what type of circumstances might you pull money out of your retirement plan to pay for something? The correct answer is ‘Never!”

7. How do you define “lifetime financial success”?

8. Do you plan to learn about investing so you can do it yourself or do you plan to hire a professional? If the former, who will manage the investments?

CHILDREN AND THEIR COLLEGE EXPENSES

1. How many children do you plan to have, and when will you start?

2. Will either spouse stay at home with the children?

3. If so, at what point will the stay-at-home spouse return to work?

4. Will one spouse homeschool the children?

5. How do you plan to pay for children’s college or career training? At what child’s age will you start saving?

TAXES

1. For most families, here are the five broad types of federal income tax deductions:

• Home mortgage interest.

• Home real estate taxes.

• Employer-sponsored, non-Roth retirement plan contributions.

• State and local income taxes.

• Charitable contributions.

Which of these might you pursue?

2. Do you plan to file your own tax returns or hire a professional? If the former, who will fill out the tax returns each year?

We will have our final list of questions next month.

• Not insured by any bank or government • Subject to risk & possible loss of principal

Our Financial Bad Boy This Month

Fraudsters who file a tax return in your name with your SS number and steal your refund.

So, how do you protect yourself?

Sign up for the new federal government’s Identity Protection PIN (IP PIN).

How do I sign up?

Google “Identity Protection PIN” or go to the following IRS website:

https://www.irs.gov/identity-theft-fraud-scams/get-an-identity-protection-pin

Scroll down half a page and click on the blue box, “Get an IP PIN”.

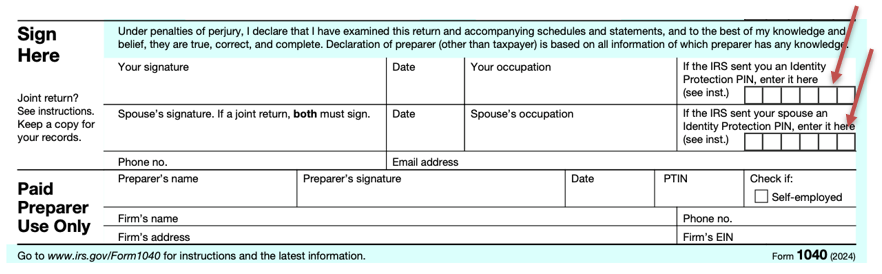

Once you get your 6-digit IP PIN, where do you enter it on your federal tax form?

The picture below is the bottom of page 2 of the IRS form 1040. Enter your 6-digit IP PIN at

the red arrows. If you are married, have your spouse get an IP PIN also.

You will get a new IP PIN every January by mail. We recommend getting an IP PIN now, even if you have already filed your 2024 return. Getting the IP PIN now will automatically get you a new IP PIN in January 2026 to be used on your 2025 tax return.

If you have obtained an IP PIN and you or a fraudster files a return without the correct IP PIN, your tax return will not be processed!

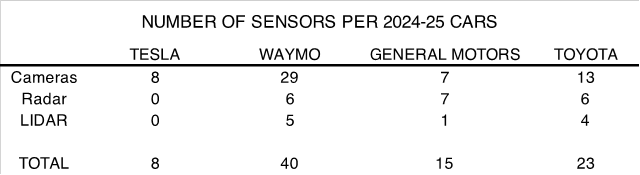

EV MANUFACTURER’S APPROACH TO SAFE AUTONOMOUS DRIVING

It’s too early to say which of the following methods are better than the others or even acceptable, but here are some facts regarding how Tesla, Waymo (an Alphabet company), General Motors, and Toyota are making autonomous driving safe.

Cameras use visible light to detect objects around the car. Supposedly, they can also see in the dark.

A radar sensor uses radio waves to measure the distance between objects. Radar sensors are effective even in rain, snow, fog, smoke, dust, and sun glare.

LIDAR stands for Light Detection and Ranging. A LIDAR sensor uses a pulsed laser to measure distances between the sensor and another object.

What’s important is not just how many sensors are on a vehicle but each sensor’s capability and the capability of the software that analyses the sensor’s data. Obviously, three of the companies above use multiple systems to create the safest system possible. Autonomous driving needs to be “safer than a human driver”, not “just as safe as a human driver”.

The Bond Market

Commentary

This month we are hearing from Jan Hatzius, Goldman Sachs Chief Economist.

Hatzius commented on the employment report that came out on June 6, saying, “There is economic slowing underneath the surface – it just isn’t dramatic. You do have some weakness in the (fewer) number of people who are quitting their jobs, and there is some updrift in the number of unemployment claims.”

“I do think we are seeing some signs of a de-acceleration of the economy, but again, it’s not dramatic. There are no signs the economy is entering a recession.”

“I think it’s going to take quite a while for the Fed to bring down interest rates. It’s a very high probability the next move is ‘down’. But for now, ‘wait and see’ is the correct expectation. In our base case of the economy, we don’t see an interest rate cut until December.”

“Regarding tariffs, we expect we will see a 1% increase in inflation in the short-term. We also see that being short lived and for sequential inflation to quickly come back down.”

“For 2nd quarter, we see GDP annual growth of 3.3%. We have odds of a near-term recession slowly dropping. But the tariff uncertainty continues to be very significant. We have not seen any meaningful trade deals. Concluding at least one major trade deal would significantly lessen the uncertainty.”

Recommended Action for Your Safest Money

Our recommendations for an investor’s safest money have changed since last month. We are dropping our recommendation for short-term, high-yield bond funds and adding bank CDs, Treasury bills and notes, and high yield savings and money market accounts.

Our recommendations, in no particular order, are:

- Short-term U.S. Investment-Grade Corporate or Securitized bond funds.

- FDIC-protected bank CDs paying at least 4%. Some banks are paying almost nothing.

- US Treasury Bills of one year, or Treasury Notes of two to five years.

- Bank or brokerage-house high-yielding savings accounts or money market accounts.

- U.S. Savings I-Bonds which have a max contribution of $10,000 per account per year, are tax deferred for 30 years, interest is credited and compounded monthly, they do not drop in value even when interest rates go up, and their interest rates vary every six months based on inflation.

Due to the relatively low return of these investment products, investors should not put 100% or anything close to that in these products. These products are only for an investor’s safest money, or perhaps 5% to 25% of an investor’s total portfolio. These products are credit safe, but they will not provide the growth or income needed to stay ahead of, or even keep up with, taxes and inflation.

Past performance is not a guarantee of future results.

Pop Quiz Answer

Since World War II (80 years ago), how many times has the S&P 500 Index dropped by the following percentages from a recent high?

Answer:

Therefore, it is normal for the stock market to drop between 5% and 10% almost every year!

What about those three times the market dropped more than 40%? What happened?

During 1973-74, the S&P 500 index dropped 48%. It was at this time Mark made his first stock market investment as a teenager and lost 50%. Even though I was perplexed by the results, I was undeterred and knew investing in the stock market was the best path for me to build significant wealth over the long term. That bear market was caused by the combination of the Arab oil embargo, rising inflation, and the aftermath of Watergate.

During 2000 to 2003, the S&P 500 Index dropped 49% while the Nasdaq dropped 78%! This bear market was caused by the Dot-Com bubble (too many tech companies with no intellectual property and no profits were finally being punished instead of being rewarded), corporate scandals involving Enron and WorldCom wrecked confidence in the system, and the September 11, 2001 terrorists attacks. The latter caused the stock market to be closed for 4 working days.

The Financial Crisis from 2007 to 2009 caused the Great Recession and a 57% drop in the S&P 500 Index. This bear market was caused by excessive and reckless mortgage lending, a collapse in housing prices, and excessive leverage at some Wall Street firms. This led to the bankruptcies of Lehman Brothers and Washington Mutual. Also, General Motors and Chrysler declared bankruptcy. In all cases, stockholders received zero. Furthermore, Bear Stearns was taken over by JPMorgan, Merrill Lynch was taken over by Bank of America, and AGI was bailed out when the US government gave them $182 billion! Mark would have let AGI sink.

Obviously, it takes multiple events to cause a 40% drop in the stock market. We probably have not seen the last one. So, when the next 20% to 40% drop comes along, just buckle your seat belt and show extraordinary courage and patience. Even during the Great Depression, the stock market did not go to zero. Some individual stocks went to zero, but the market as a whole did not.