Welcome to the August 2025 Newsletter. This month, we’re discussing the economy, employment, financial terminology, and more.

Summary

On July 23, Jeremy Siegel, Professor of Finance at the Wharton School said, “Things are looking good. The trade agreement with Japan, and it looks like it is going to be extended to the EU, is about as good as the market expected. And all of this optimism will keep the stock market moving higher.”

“Yes, the forward PE ratio of the S&P 500 Index is about 22 – and it’s on the high side. But the forward PE of the Magnificent 7 is in the 30’s while the forward PE of the remaining 493 stocks is around 19 – which is not extreme. This is not a market that is challenged. The biggest issue is, are AI companies going to keep up with the rest of the market? It looks like they will.”

“Our short-term interest rates should be in the three’s and not in the four’s. So, if or when we get short-term interest rates down in the three’s, it’s blue skies ahead!”

Quote of the Day

Jeanne Sinquefield is the former Executive VP of Dimensional Fund Advisors. Her responsibilities included portfolio management, trading, and new employee orientation.

Sinquefield would tell the firm’s new employees, most of whom had PhD degrees, “When you have a PhD, you learn more and more about less and less until eventually you know everything about nothing.”

“Those with an MBA learn less and less about more and more until eventually they know nothing about everything.”

I have both a PhD and an MBA, so I know everything about everything”. The new employee’s typical response was, “Yes ma’am.” At the completion of orientation, all the new employees knew exactly who was in charge.

Pop Quiz

At the most basic level, what is the job of our US Representatives and Senators in Washington, DC?

The answer to this month’s Pop Quiz is at the bottom of the newsletter.

The Economy

Employment

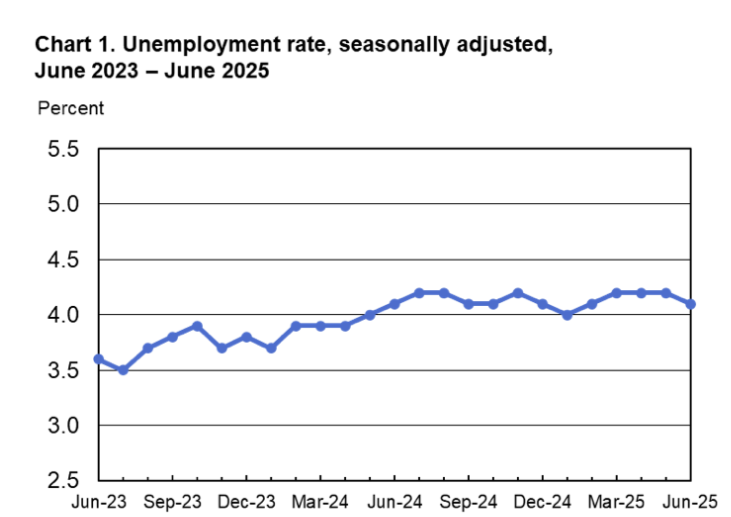

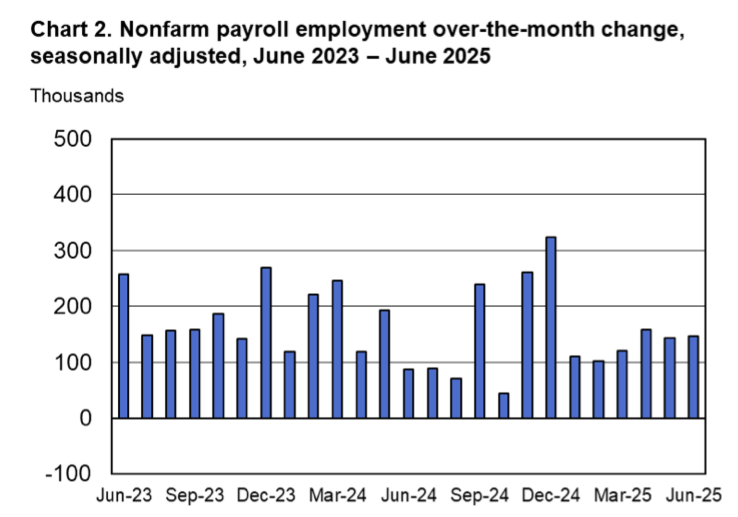

Total U.S. nonfarm payroll employment rose by 147,000 in June. The official unemployment rate, U-3, dropped slightly to 4.1%. The April and May 2025 combined employment numbers were revised higher by 16,000 than previously reported.

Chart 1 below is based on the Bureau of Labor Statistics official unemployment rate, U-3.

Chart 2 below shows the two-year trend of employment growth.

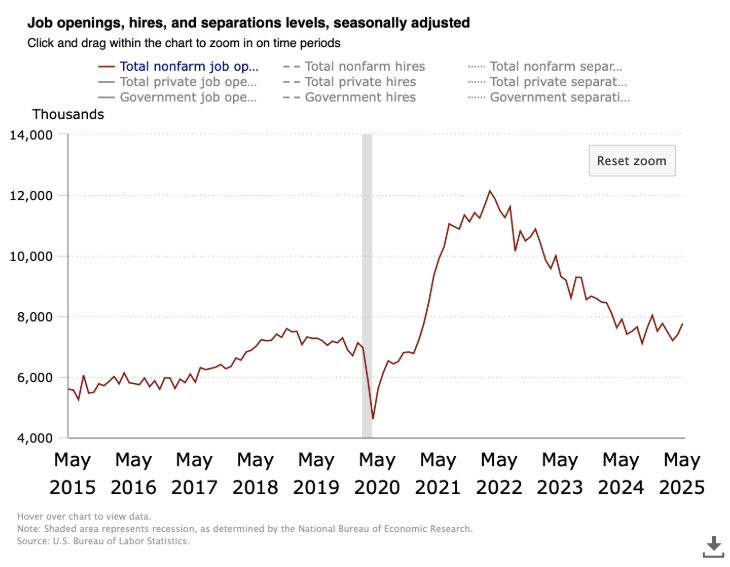

The Job Openings & Labor Turnover Survey (JOLTS) increased slightly to 7.8 million open jobs across the country as of the last business day in May. It was 7.4 million in the prior month. The 10-year chart below shows that the downward trend has continued in open jobs since March 2022.

The seasonally adjusted Total U.S. Unemployment Rate, U-6, remained the same at 7.7% in June as compared to the prior month. There were 7.5 million people unemployed in June, aged 16 and older. Last month, it was 6.8 million people unemployed.

June Unemployment Rates by Education Level

Average hourly earnings of all employees on private nonfarm payrolls were up 3.7% in June compared to a year ago. It was 3.9% the previous month.

| Less Than High School Diploma | 5.8% |

| High School Graduate, No College | 4.0% |

| Some College, Associate's Degree, or Skilled Trade Degree | 3.2% |

| Bachelor's Degree or Higher | 2.5% |

Leading Economic Indicators (LEI) sponsored by The Conference Board

The LEI decreased 0.3% in June after a revised “no change” in May. The Conference Board’s spokesperson said, “For a second month in a row, the stock market rally was the primary support for the LEI. But this was not enough to offset very low consumer expectations, weak new orders in manufacturing, and a third consecutive month of rising initial unemployment claims.”

Gross Domestic Product (GDP)

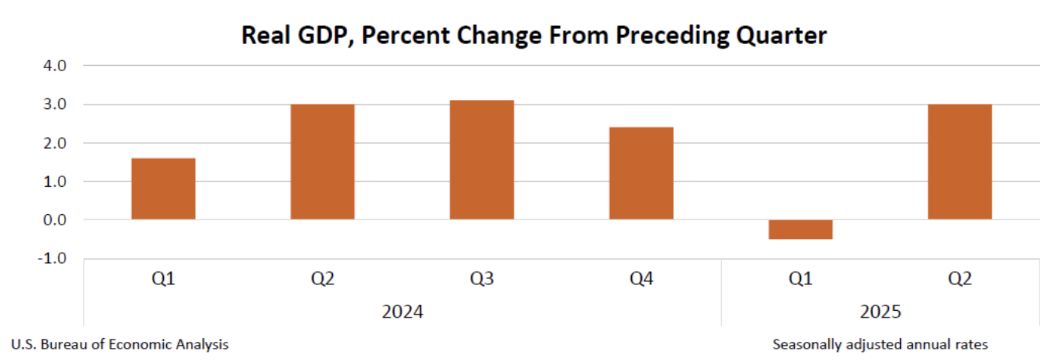

The Bureau of Economic Analysis said the first estimate for GDP in the second quarter of 2025 increased at a significant annual real rate of 3.0%! GDP for the first quarter of 2025 was -0.5%.

The increase in the second quarter GDP reflected a decrease in imports, which is a subtraction in the GDP calculation, and an increase in consumer spending. For the year 2024, GDP increased 2.8% and grew 3.2% in 2023.

Labor Productivity – Second Quarter data will be released in August.

Annualized and seasonally adjusted, nonfarm labor productivity was a disappointment by decreasing by a revised 1.5% in the first quarter of 2025 as reported by the Bureau of Labor Statistics. The original report had labor productivity decreasing by 0.8%. For the same quarter a year ago, labor productivity increased 1.4%.

By calendar year, labor productivity grew a revised 2.8% in 2024 and 1.9% in 2023.

Inflation

Annual inflation increased to 2.6% as measured by the Personal Consumption Expenditures (PCE) price index for June. The revised annual May number was 2.4% during the prior 12 months. The annual core PCE price index, which excludes food and energy, remained at 2.8% in June. It was 2.8% in May.

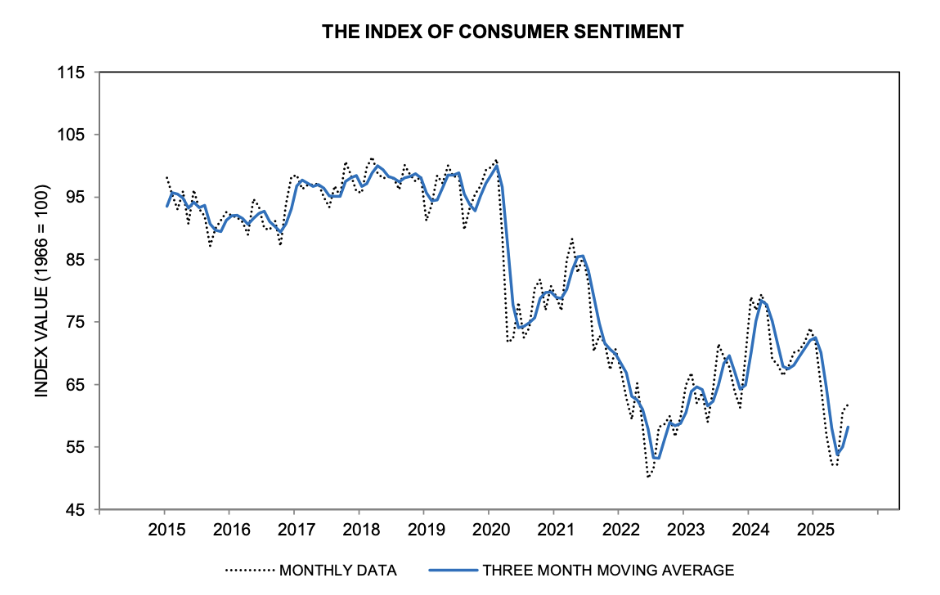

University of Michigan Consumer Sentiment

Consumer sentiment in July rose to 61.8 compared to June’s revised 60.7. See the 10-year chart below.

Consumers are unlikely to regain their confidence in the economy unless they feel assured that inflation is unlikely to worsen – for example, if trade policy stabilizes. At this time, personal interviews have revealed little evidence that other policy developments, including the recent passage of the tax and spending bill, have moved the needle much on consumer sentiment.

Mortgage Rates and Average Existing Home Prices

As of July 30, 2025, the average 30-year fixed-rate mortgage had an interest rate of 6.77%, compared to 6.82% last month. The average 15-year fixed rate mortgage had an interest rate of 6.03%, compared to 6.04% last month.

The median existing single-family home sale price increased in June 2025 to $441,500 from $432,800 in June 2024. The volume of existing home sales increased 0.6% compared to a year earlier, according to the National Association of Realtors. The inventory of existing homes for sale decreased by 0.6% compared to May. This represents a 4.7-month supply of homes for sale. The desired supply target is 6 months.

The U.S. Public Debt as Issued by the Treasury Department as of July 30, 2025, was:

$37,169,000,000,000.

Last month it was $37,030,000,000,000.

Important Dates in August

THE STOCK MARKET

Commentary

On July 23, Lauren Goodwin, New York Life Chief Market Strategist and Economist, spoke on CNBC, saying, “We are starting to see inflation creep into the economic data. I expect inflation to accelerate into Q3 and Q4 because new ordering, especially for the Christmas holidays, has only just started.”

“The labor market is starting to tighten due to a decrease in immigrants. This can impact inflation later this year. We don’t have an overly bearish view of the US economy. I think the Fed might cut rates one time this year.”

“Regarding the key sectors of the S&P 500 Index, here are my thoughts.”

“Technology: AI firms will likely remain the key growth engines”.

“Financials: Banks have defied cautious headlines and now they have an upbeat to earnings.”

“Industrials: Firms are getting a boost from robust backlogs, increases in defense spending, and improving supply chains”.

“Consumer Discretionary: These businesses face a tough landscape with price-sensitive consumers.”

Just remember, how do life insurance companies invest? Very conservatively – too conservatively, we believe, for most investors.

Stock Market Valuation

On July 21, Jonathan Krinsky of BTIG said, “The NASDAQ 100 (100 largest tech stocks in the US) has now gone 60 trading days without closing below its 20-day moving average – the second longest streak in history. The main takeaway is, we may encounter some turbulence (a short-term correction of 5 to 10%) even though this is unlikely to mark a major peak.”

On July 8, four brokerage houses increased their outlook for the S&P 500 Index as below.

Year-End Targets

Bank of America’s Merrill raised their S&P 500 Index year-end target to 6,300 from 5,600.

Goldman Sachs raised their S&P 500 Index year-end target to 6,600.

Fundstrat Global Advisors raised their S&P 500 Index year-end target to 6,800.

Forward Looking Next 12-Month Targets

Bank of America’s Merrill raised their S&P 500 Index 12-month target to 6,600.

The Bank of Montreal raised its S&P 500 Index 12-month target to 6,700.

Goldman Sachs raised their S&P 500 Index 12-month target to 6,900 from 6,500.

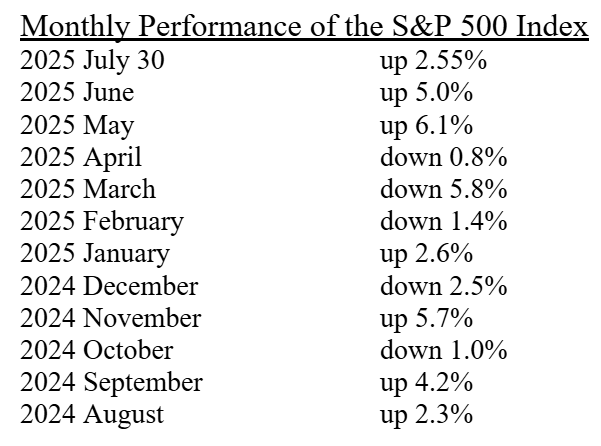

The S&P 500 Index closed on July 30, 2025, at 6,362.90. Year to date, the market is up 8.2%.

Prior Annual S&P 500 Performance As Per The Exchange Traded Fund, VOO

2024: +24.98%

2023: +26.32%

2022: -18.19%

2021: +28.78%

2020: +18.29%

2019: +31.35%

Recommended Action for Your Stock Portfolio

During July, various commentators on CNBC listed major themes regarding “what is going on in the world” as possible opportunities for investing. They are listed here in no particular order:

- Artificial intelligence

- Cyber security

- US Infrastructure needing to be updated or replaced.

- Energy expansion and transition.

- Global labor shortage.

- Immigration.

- New health care products and diagnostic testing innovations.

- US online retail domination by Amazon, Walmart, and Costco.

- Aging population within all industrialized countries.

WARNING: Individual investing has become more treacherous as brokerage houses have invented more and more high-cost, high-risk products so they can make more money but not so much for the average investor.

∙ Not FDIC Insured ∙ No Bank Guarantee ∙ May Lose Value

Financial Markets Vocabulary

Your FICO Score is based on the following:

- Payment History 35%

- Amount Owed 30%

- Length of Credit 15%

- Credit Mix 10%

- New Credit 10%

TOTAL 100%

Last month, we discussed “Payment History” and “Amount Owed”. This month, we are reviewing the latter three criteria.

Length of Credit – This considers how long a person has had a credit account open, the age of your oldest account, the age of your newest account, and the average age of all your accounts.

Credit Mix – This refers to the variety of credit accounts you have, which may include credit cards, retail accounts, installment loans, and mortgages.

New Credit – This considers the number of new accounts a person has opened recently and the number of recent credit inquiries, which can be seen as a sign of greater risk if a person opens multiple accounts in a short period, particularly for those with short credit histories.

OK, Now What Do I Do?

Financial Questions for Engaged Couples

This is our final installment of our four-month series of appropriate financial questions for engaged couples. Parents and grandparents, please get involved!

LONG-TERM FINANCIAL GOALS

1. What are your individual long-term financial goals?

Some valid answers are a fully funded emergency fund, home ownership, no debt except a conventional, fixed-rate, first-mortgage on your primary residence, having all appropriate insurance, saving for kids' college, and saving 15% of gross income for retirement.

2. Do cars and trucks appreciate or depreciate? Answer: Depreciate

Do homes appreciate or depreciate? Answer: Appreciate

Therefore, do not overspend on cars and trucks. One rule of thumb: add up the current value of all things owned that have a motor (car, truck, riding lawn mower, jet ski, snowmobile, fishing boat, etc.) should not equal more than 50% of the family’s annual income.

3. Who should a person not accept financial advice from?

Answer: Don’t bother taking financial advice from anyone who is broke.

HOME OWNERSHIP

Not counting repairs and maintenance, what is the maximum a family should spend monthly to own a single-family home?

Answer: Principal, interest, real estate taxes, homeowner’s insurance, and private mortgage insurance if any, but hopefully not, should not exceed 25% of the take-home pay of the family.

ESTATE PLANNING

Everyone over the age of 18 needs the following five documents. For a married couple, this is a total of 10 documents!

- Will

- Durable Power of Attorney

- Health Care Power of Attorney (if you are unconscious, this document names who can make medical decisions on your behalf).

- Health Care Directive (Also called a living will. If you are terminal and unconscious, how do you want to be treated – feeding tube, pain killers, fluids?)

- HIPAA Release (With whom can hospitals and doctors share your medical information).

Do you have these documents today? If not, when do you plan to get them?

An optional document is a Revocable Living Trust. This can cost as much as the other five documents combined.

CONTINUING EDUCATION

When will you both attend Dave Ramsey’s 9-week Financial Peace University?

AT A VERY HIGH LEVEL, BEFORE DEBT REDUCTION OR SAVING FOR A HOME CAN TAKE PLACE, WHAT MUST A FAMILY ALWAYS PAY FOR FIRST?

Answer:

- Home mortgage/rent

- Utilities

- Food

- All taxes

- All insurance

- Transportation (especially to and from work)

FINANCIAL STEPS BEFORE MARRIAGE

You have a son or daughter or grandchild in their 3rd or 4th year of college, and they have fallen in love. Now they are talking marriage. What advice should you offer?

Don’t get married until:

1. You both first graduate from college or a trade school.

2. If one or both are majoring in a profession that requires a certification exam after college, pass the exam after graduating. Examples are CPA’s, doctors, lawyers, etc.

3. Both are to get a job in their field of study. A history major getting a construction job does not count. If there are no job opportunities in a spouse’s major, switch majors NOW!

4. Both spouses are to eliminate all debt.

5. Save up a joint emergency fund of at least three months of anticipated expenses.

6. Save up for the wedding. There should be no borrowing just to get married.

7. Do not buy any assets together (cars, home, etc.) until after marriage.

FINANCIAL STEPS AFTER THE HONEYMOON?

1. Get your estate planning documents in place.

2. Don’t loan money to anyone. Don’t co-sign loans for anyone. If you want to financially help someone, GIVE them some money, no loans. One stipulation you might want to use is, “Here are x dollars. This is a gift, not a loan. We do not expect you to pay us back. But if you decide to take this gift, there is only one string attached – you can never ask us for money again.”

• Not insured by any bank or government • Subject to risk & possible loss of principal

Our Financial Bad Boy This Month

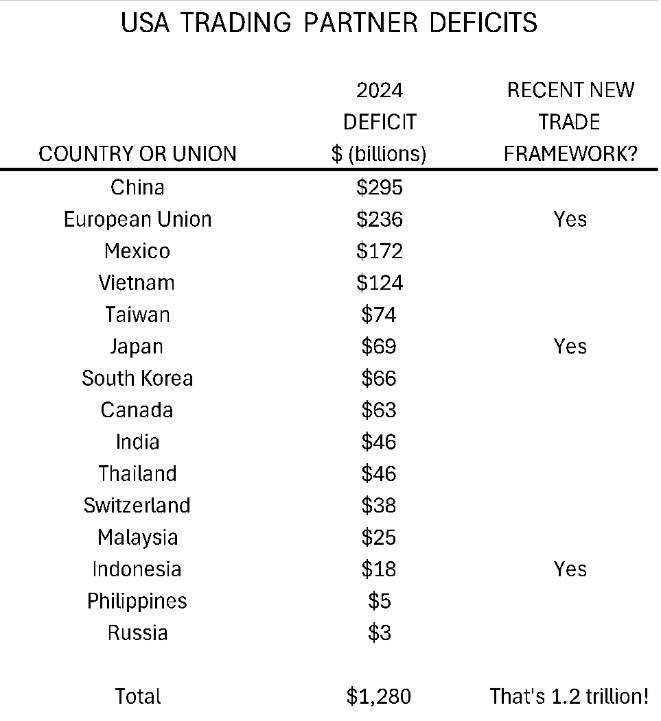

As new trade agreements are in the news, we thought it timely to show the top 15 countries the US has a trade deficit with.

The US has had for a number of years “Trade & Investment Framework Agreements” with over 75 countries. These older agreements have tolerated and sanctioned the $1.2 trillion annual trade deficit.

The Bond Market

Commentary

On July 16, Morgan Stanley said regarding the U.S. economic outlook, “We continue to expect the strongest inflation push from tariffs will be in August. Meanwhile, slower immigration puts downward pressure on the unemployment rate. We believe the Fed is on hold for the remainder of this year. We expect they will begin cuts in March 2026 and cut by 25 basis points at every meeting thereafter” (until they reach their predicted neutral rate).

On July 30, the Federal Open Market Committee announced they are keeping its policy interest rate at 4.25% to 4.50%, with no change. Their next meeting is in September.

Recommended Action for Your Safest Money

Our recommendations for an investor’s safest money have not changed from last month. Our recommendations, in no particular order, are:

Our recommendations, in no particular order, are:

- Short-term U.S. Investment-Grade Corporate or Securitized bond funds.

- FDIC bank CDs paying at least 4%. Some banks are paying almost nothing.

- US Treasury Bills of 1 year, or Treasury Notes of 2, 3, or 5 years.

- Bank or brokerage-house, high-yield savings or money market accounts (4% min.).

- U.S. Savings I-Bonds have a max contribution of $10,000 per account per year, are tax deferred for 30 years, do not drop in value even when interest rates go up, interest is paid and compounded monthly, and their interest rates vary every six months based on inflation.

Due to the relatively low return of these investment products, investors should not put 100% or anything close to that in these products. These products are only for an investor’s safest money or perhaps 5% to 25% of an investor’s total portfolio. These products are credit safe, but they will not provide the growth or income needed to stay ahead of, or even keep up with, taxes and inflation.

Past performance is not a guarantee of future results.

Pop Quiz Answer

At the most basic level, what is the job of our US Representatives and Senators in Washington, DC?

Answer:

Their job is to “show up, listen, investigate, talk, debate, negotiate, compromise, and vote.” If a member of Congress cannot do these things, they are in the wrong job!