Welcome to the April 2026 Newsletter. This month, we’re discussing the economy, employment, financial terminology, and more.

Summary

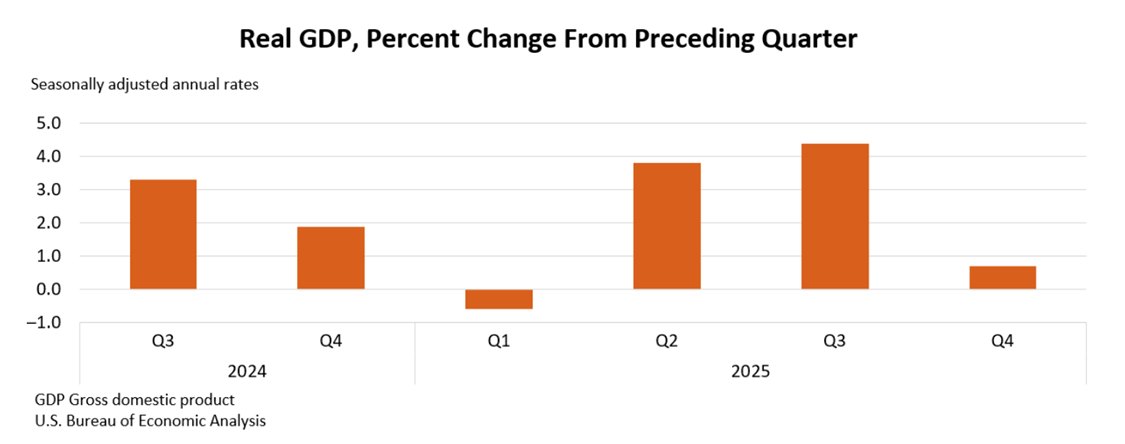

The economy could be better. Fourth quarter labor productivity was dismal at 1.5%, and fourth quarter GDP was terrible at only 0.7%. This was all because of the government shutdown – great job, Congress! Fortunately, average weekly unemployment initial claims, a leading indicator, shows strong evidence that a recession is not imminent. It is reasonable to expect first quarter 2026 data will be better, and so will the second quarter data. Now is the time to show patience.

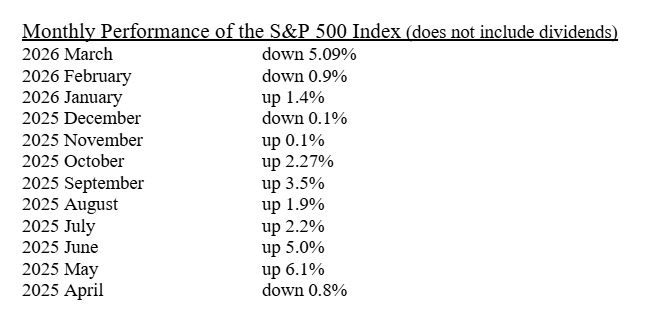

The S&P 500 Index had its all-time closing high on January 27, 2026, at 6,978.6. On March 30, 2026, the index closed at 6,343.72. This represented a decline of 9.1%. On March 31, the index was up 2.92% so perhaps this correction is over, but we will have to wait and see. If March 31 was only a one-day pop and we are headed back down, Wall Streeters will call March 31 a “dead cat bounce”.

But we are optimistic for both the economy and the stock market, especially in the intermediate-term and the long-term.

Quote of the Day

On March 23, 2026, Dave Ramsey was ranting to a caller whose spouse was day-trading stocks. Dave described that action as extremely foolish. Dave said in part, “Studies have shown that people who day-trade daily for months at a time have a 97% chance of losing money!”

TWO PREVIOUS INVESTING QUOTES BY WARREN BUFFETT

Some of the best investing advice has come from Buffett in his annual letters to investors. These included, “Never bet against America.”

Another was, “We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.”

Pop Quiz

Who said the following?

“With malice toward none, with charity for all, with firmness in the right, as God gives us to see the right, let us strive on to finish the work we are in, to bind up the nation’s wound, to care for him who shall have borne the battle, and for his widow and orphans; to do all which we may achieve and cherish a just and lasting peace among ourselves and with all nations.”

The answer to this month’s Pop Quiz is at the bottom of the newsletter.

The Economy

Employment

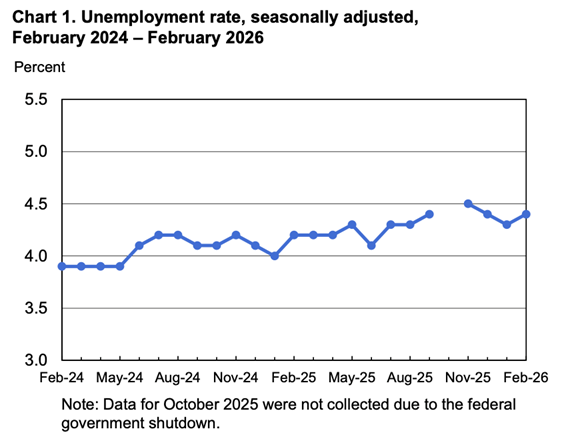

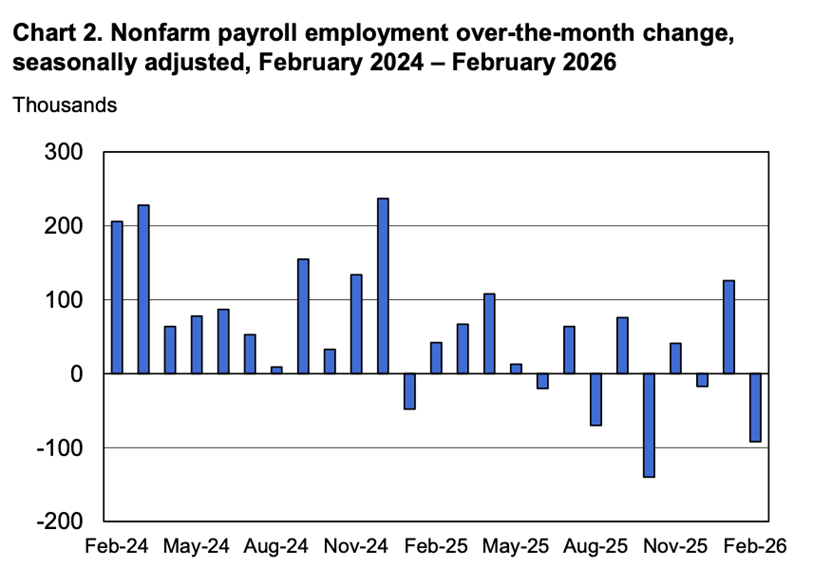

Total U.S. nonfarm payroll employment dropped by 92,000 in February. The official unemployment rate, U-3, increased to 4.4%. The December 2025 and January 2026 combined employment numbers were revised lower by 69,000 than previously reported.

Chart 1 below is based on the Bureau of Labor Statistics official unemployment rate, U-3.

Chart 2 below shows the two-year trend of employment growth.

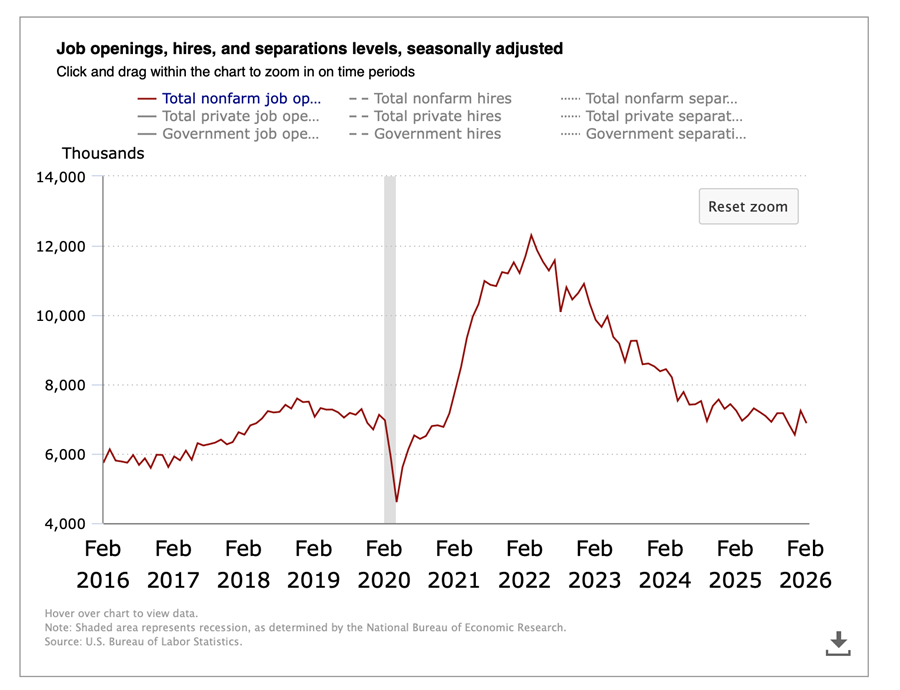

The Job Openings & Labor Turnover Survey (JOLTS) decreased to 6.9 million open jobs across the country as of the last business day in January. It was 7.1 million in November. The 10-year chart below shows the downward trend continues in open jobs since March 2022.

The seasonally adjusted Total U.S. Unemployment Rate, U-6, decreased to 7.9% in February as compared to 8.1% in January. There were 8.1 million people unemployed in February, aged 16 and older. In January, it was 7.9 million people unemployed.

February Unemployment Rates by Education Level

Average hourly earnings of all employees on private nonfarm payrolls were up 3.8% in February compared to a year ago. It was 3.7% in January.

| Less Than High School Diploma | 5.6% |

| High School Graduate, No College | 4.8% |

| Some College, Associate's Degree, or Skilled Trade Degree | 3.5% |

| Bachelor's Degree or Higher | 3.0% |

Gross Domestic Product (GDP)

The Bureau of Economic Analysis said the second estimate for GDP in the fourth quarter of 2025 increased at an annual real rate of only 0.7%.

The increase in the fourth quarter GDP reflected an increase in consumer spending and investment. These increases were offset by decreases in government spending and exports. For the year 2025, GDP increased by 2.1%, in 2024 GDP increased by 2.8%, and grew 3.2% in 2023.

Leading Economic Indicators (LEI) sponsored by The Conference Board

The LEI declined by only 0.1% in January after a revised decrease of 0.2% in December. The Conference Board’s spokesperson said, “While the topline LEI continues to signal headwinds to economic activity, the strengths among its components during the next six-months were up on a widespread basis with 7 out of 10 components advancing.”

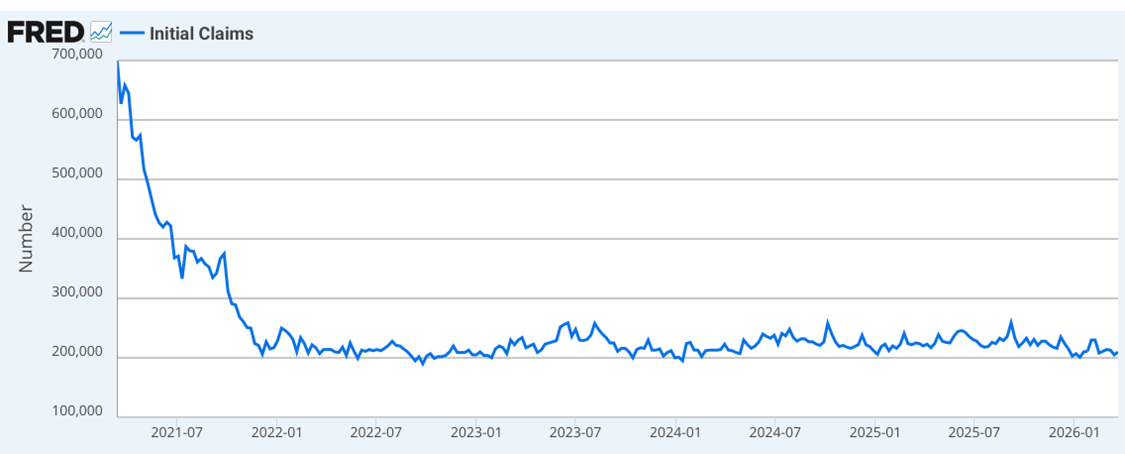

The 4-Week Moving Average of Unemployment Initial Claims is Another Leading Indicator

The week of March 26 initial unemployment claims came in at 210,000. See the 5-year chart below from the St. Louis Federal Reserve Bank. The higher the graph, the more likely a recession is coming.

With the number of initial unemployment claims hovering around 200,000 per week, there is no recession in sight! The high number of initial unemployment claims on the left of the chart was the result of the Federal Reserve increasing interest rates seven times in 2022. This resulted in an economic contraction in 2022 and significant labor layoffs that began in mid 2021.

Labor Productivity (quarterly releases only)

Annualized and seasonally adjusted, nonfarm, labor productivity increased by 1.5% in the fourth quarter of 2025 as reported by the Bureau of Labor Statistics. For the year 2025, labor productivity increased at an annual rate of 2.1%.

By calendar year, labor productivity grew 2.3% in 2024 and an anemic 1.6% in 2023.

Inflation

Annual inflation decreased slightly to 2.8% as measured by the Personal Consumption Expenditures (PCE) price index for January. The revised annual December number was 2.9%. The annual core PCE price index, which excludes food and energy, increased slightly in January to 3.1% from 3.0% in December.

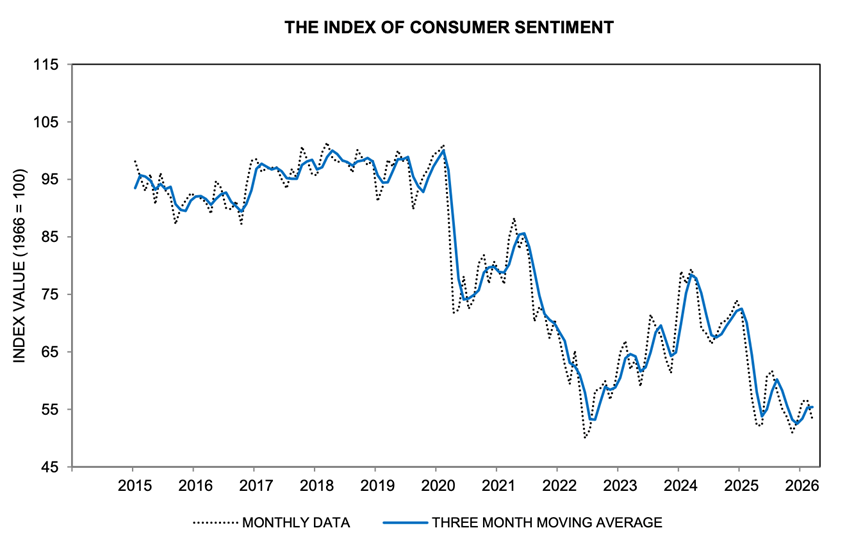

University of Michigan Consumer Sentiment

Consumer sentiment in March decreased to 53.3 compared to February’s revised 56.6. See the 10-year chart below.

Following the beginning of the Iran War, large drops in consumer sentiment began to develop. Short-run economic outlook plunged, and year-ahead expected personal finances sank, while the decline in long-run expectations was more subdued. These patterns suggest that consumers may not expect recent negative developments to persist far into the future.

Mortgage Rates and Average Existing Home Prices

As of March 31, 2026, the average 30-year fixed-rate mortgage had an interest rate of 6.47% compared to 5.99% last month. The average 15-year fixed rate mortgage had an interest rate of 6.03%, compared to 5.60% in the previous month.

The median existing single-family home sale price increased in February 2026 to $401,800. That was up 0.2% compared to 12 months earlier. The seasonally adjusted annual rate of existing home sales decreased 1.1% compared to a year earlier, according to the National Association of Realtors. The inventory of existing homes for sale increased by 4.9% compared to February 2025. This represents only a 3.6-month supply of homes for sale.

The U.S. National Debt as Issued by the Treasury Department as of March 31, 2026, was:

$39,059,000,000,000.

Last month it was $38,743,000,000,000.

Important Dates in April

THE STOCK MARKET

Commentary

The best thing driving this stock market up is that corporate profits are strong. Unfortunately, there is more than one negative drag on the market. These include the Iran War, oil priced around $100 a barrel, there is a total frustration by investors regarding the private credit market because the investors can only get about 5% of their money out per quarter, the Fed has stopped dropping interest rates, and way too many investors have become scared of artificial intelligence (AI) thinking it is going to put all the software companies out of business. What a farce that last one is.

I challenge anyone in the press who is promoting this idea by naming one S&P 500 CEO, chief IT officer, or board member who is advocating, “Lets jerk out our cybersecurity software and let AI protect our data.”

So yes, there are some really stupid people in the press and on Wall Street. (AI told me I should not say stupid but instead say ill-advised or just call those people a ‘pudden-head’.)

What sectors do we think are likely to grow moderately to fast the rest of this year?

- Data center construction

- Upgrading the 50-year-old electrical grid

- Adding more power plants

- Cybersecurity software

- Retail dominated by Amazon, Walmart, and Costco

- The magnificent seven stocks

- Chip manufacturers

- Chip equipment manufacturers

- And the highly profitable industrial, health care, energy, and financial companies

Stock Market Valuation

Tom Lee, Head of Research at Fundstrat Global Advisors, commented on March 20 regarding his expectation of where the S&P 500 Index would end in 2026. Lee refused to lower his expectations for the index. He previously predicted it would end the year at 7,700. He reiterated this target again today on CNBC.

On March 17, Ed Yardeni, President of Yardeni Research, said on CNBC he is maintaining his year-end prediction for the S&P 500 to reach 7,700.

The S&P 500 Index closed on March 31, 2026 at 6,528.52. Year to date, the Index, as per the exchange-traded fund, VOO, is down 4.41%. This fund includes dividends.

• Markets are volatile • Always consult your financial advisor before investing

Recent Annual S&P 500 Performance As Per The Exchange Traded Fund, VOO

2025: +17.82%

2024:+24.98%

2023: +26.32%

2022: -18.19%

2021: +28.78%

2020: +18.29%

2019: +31.35%

Recommended Action for Your Stock Portfolio

It has been a long time since we talked about investing in international stocks. But we have recently found an exchange-traded fund (ETF) that might be a good start. It is IVLU, iShares Edge International Value.

This ETF is a large-cap, international value stock fund rated by Morningstar as 5-star, Gold. Noting that international funds always have a higher expense ratio than similar US funds, the annual expense ratio of IVLU is a reasonable 0.31%. The average annual return of this fund over the past 5 years has been 13.01%.

Comparing this fund to other funds in the same category, Morningstar rates this fund as having an average risk with a high return. This fund does not hedge it foreign currencies against the US dollar. Therefore, the total return of this fund depends on the prices of the underlying international stocks within the fund and the fluctuations of foreign currencies compared to the US dollar.

∙ Not FDIC Insured ∙ No Bank Guarantee ∙ May Lose Value

Financial Markets Vocabulary

Let’s talk about “risk”. Also, please recognize that the word “volatility” can be substituted for the word “risk”.

Risk is one of the most important concepts we need to learn about ourselves. Invest too aggressively for your personality, and if you get burned, you might erroneously conclude, “The stock market is for fools!”

Invest too conservatively, and you might end up with a less than a desirable retirement, or an inability to buy your first home or pay for your children’s college.

If you are likely to give a “deer in the headlights look” when a financial advisor asks you, “What is your risk tolerance?”, perhaps these on-line questionnaires will help.

Search for the following.

- Vanguard Investor Questionnaire

- Charles Schwab Investor Profile questionnaire

- Merrill Edge Risk Tolerance Quiz

- Investment Risk Tolerance Assessment by the University of Missouri

These tests typically analyze two distinct factors: your willingness to take risk (how you feel about market drops) and your capacity for risk (your financial ability to lose money without impacting your lifestyle).

We suggest everyone take one or more of these quizzes to help determine, to the best of their ability, what their risk tolerance is. When you are comfortable acknowledging your own risk tolerance, put a number on it from 1 to 100, with 100 meaning you want 100% of your portfolio invested in the stock market, and a 60 meaning 60% in the stock market, etc. Then you or your advisor can implement an asset allocation of stocks, bonds, and cash that is perfectly appropriate for you. As you get older, most people will want to lower their allocation to stocks to reduce their portfolio’s volatility.

OK, Now What Do I Do?

Referring back to the Quote of the Month, Dave Ramsey said do not do anything close to “day-trading” in the stock market. So how should one invest?

At Lorenz Financial we believe substantial wealth can be built over a lifetime by investing as follows:

- Spend less than you make and invest the difference.

- Max out a Roth IRA each year for you and a spouse. This is allowed even if only one spouse is working.

- Take full advantage of an employer’s retirement plan, especially if they offer a match.

- Start investing early as money invested in your 20’s has 40 years to grow while money invested in your 50’s only has 10 years to grow.

- As quickly as possible, annually increase your retirement savings until you are investing 15% of your gross income.

- Be a long-term investor and not a short-term trader.

- Build a portfolio that is highly diversified, very low cost and tax efficient (for taxable accounts).

- For nine out of 10 people, the place to build lifetime wealth will be either the stock market or real estate, not bank CD’s, money market accounts, or short-term bond funds.

- Permanently eliminate all bad debt. All debt is bad debt except for a fixed-rate, first mortgage on your primary residence. Stop wasting money by paying interest on debt.

- Build an emergency fund of 3 to 6 months of living expenses.

- Avoid the possibilities of a financial disaster hitting your family by having all the appropriate insurance (health, home or renters, auto, umbrella liability, term life, ID theft protection, long-term disability income, long-term care insurance purchased between ages 55 to 60).

- Minimize money spent on assets that depreciate (anything with wheels or an engine). Total dollar value of these assets should not be more than 50% of the family’s annual income.

∙ Not insured by any bank or government ∙ Subject to risk & possible loss of principal

OIL AND NATURAL GAS WORLDWIDE PRICING

If the price of oil in Europe is $100 a barrel, for the same grade of oil, the price is the same in the US, Kuwait, Japan, China, etc. Oil has a similar international price but will vary due to the grade of the oil and the cost of transportation from point A to B.

Natural gas does not have a similar worldwide price. Why not? Because natural gas is transported domestically by pipeline in its gaseous state. This is an inexpensive process. But between continents, natural gas is first cooled to -260 deg F (-162 deg C) and loaded onto special insulated ships. Then, at the receiving port, it is heated and pumped as a gas through their pipelines. This transportation process is very expensive. For that reason, natural gas in the US might be $3.00 per million BTUs, but in Europe, where they must pay for the expensive transportation costs from the US or Qatar, the price will be double or triple that of the US.

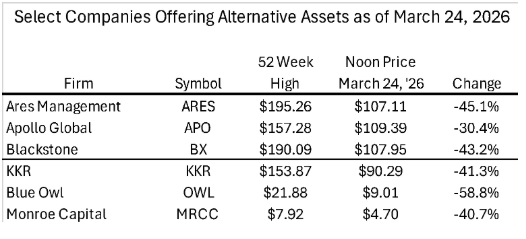

Our Financial Bad Boy This Month

This month, our bad boy is “private credit," again! Here is some recent analysis.

Here are six firms that are significantly involved in the field of alternative asset management. Alternative asset managers tend to offer clients securities in private credit, private equity, and non-traditional forms of real estate.

Lately, these types of assets have become broadly unfavorable due to high fees, lack of transparency within the security, and a lack of liquidity (inability to get your money out when you want it). Because of this, some of the companies have had their stock price decline significantly as below.

In Lorenz Financials' opinion, the category of alternative assets was invented to increase the profits of the asset managers and not to increase the profitability or to safeguard the assets of clients. Please avoid purchasing any form of alternative assets.

THE SKYROCKING PRICE OF COMPUTER MEMORY

AI is gobbling up all the memory the big three memory companies can produce. Those companies are:

- Samsung: South Korea

- SK Hynix: South Korea

- Micron: USA

For example, here is how much memory is being included with each Nvidia AI chip:

- Blackwell: 192 GB of high bandwidth memory (HBM) 3

- Blackwell Ultra: 288 GB of HBM3

- Rubin: 288 GB of HBM4

- Rubin Ultra: 1,000 GB of HBM4

Keep in mind, Nvidia is scheduled to produce 7.5 million AI chips this year!

As demand for any product goes up, so do its prices. This is why memory prices for your phone and computer have risen steeply in the past few months. For example, 16 GB of DDR5 memory has tripled in price between September and December 2025. High memory prices have become a recent black eye for AI.

The Bond Market

Commentary

On March 18, Chair Jay Powell held a news conference following the announcement by the Federal Open Market Committee that they had voted to hold short-term interest rates steady.

The vote was 11 to 1 to hold the federal funds rate in the range of 3.50% to 3.75%. The one vote was to lower short-term rates by 0.25%. Rate changes are typically 0.25%. The whole committee did signal they expected one rate cut later this year.

Chair Powell said he would retain his separate position as a Fed Governor at least until a Justice Department investigation of the central bank and of Powell himself “is well and truly over, with transparency and finality.”

Jay Powell’s chairmanship ends on May 15, 2026. His Fed Governorship term ends on January 31, 2028. President Trump leaves office on January 20, 2029.

Recommended Action for Your Safest Money

Our investor’s safest money recommendations are now listed below and in order with the top line, PRPFX, representing the potentially highest returns, is reasonably credit safe, but likely will have the highest volatility. This month, we are adding short-term US corporate high yield (junk bond) funds as an option for PART of a family’s safe money.

- Permanent Portfolio mutual fund, PRPFX, or gold or silver bullion.

- Short-term U.S. corporate high-yield, junk bond funds.

- Short-term U.S. investment-grade corporate or securitized bond funds.

- FDIC bank or NCUA credit union, 1 to 4 yr CDs, paying at least 3.9%.

- Bank or brokerage-house, high-yield savings or money market accounts, 3.8% min.

- US Treasury Bills of 1 year, or Treasury Notes of 2, 3 or 4 years.

- U.S. Savings I-Bonds which have a max contribution of $10,000 per account per year, are tax deferred for 30 years, do not drop in value like bonds drop in value when interest rates rise, interest is paid and compounded monthly, and the interest rate resets every six months based on inflation (the higher the inflation, the higher the interest rate).

The bottom option in the list above, U.S. Savings I-Bonds, are the most credit safe and have the lowest volatility but potentially the lowest returns. The seven safe money ideas above are in order, with the highest volatility items on top and the lowest volatility items on the bottom. We recommend everyone spread their “safe money” over at least five of the seven ideas above.

Due to the low return of all these investment products, investors should not put 100% or anything close to that in these products. These products are only for an investor’s safest money or perhaps 5% to 40% of an investor’s total portfolio as based on the investor’s risk profile. These products are mostly credit safe, but they will not provide the growth or income needed to stay ahead of, or even keep up with, taxes plus inflation.

Past performance is not a guarantee of future results.

Pop Quiz Answer

Who said the following? “With malice toward none, with charity for all, with firmness in the right, as God gives us to see the right, let us strive on to finish the work we are in, to bind up the nation’s wound, to care for him who shall have borne the battle, and for his widow and orphas; to do all which may achieve and cherish a just and lasting peace among ourselves and with all nations.”

Answer:

Abraham Lincoln. The quote above was the last paragraph in his 2nd Inaugural Address given on March 4, 1865. The President’s two greatest speeches of his term were the Gettysburg Address and his Second Inaugural Address

Both addresses were uncommonly short. The Gettysburg Address was delivered in 2 minutes, and the 2nd Inaugural Address was given in 6 minutes.