Welcome to the March 2026 Newsletter. This month, we’re discussing the economy, employment, financial terminology, and more.

Summary

As this is being written early on Monday, March 2, the air war with Iran began on Saturday. This will influence both the economy and the stock market in the very short-term.

The economy is improving with a few hiccups. GDP in the 4th quarter, which was much lower than expected, was heavily influenced by the government shutdown. Productivity continues to be excellent, but hiring is less than desirable. Average weekly unemployment initial claims, a leading indicator, shows strong evidence a recession is not imminent. Unfortunately, we will need to wait until mid to late April to see March’s economic numbers, which will tell us how the new war is affecting the economy.

A significant stock market surprise has been today’s (March 2) pre-market decline of 1%. During the first two days of the air war in Iraq, Thursday and Friday, January 17 and 18, 1991 to eradicate Iraqi military forces from Kuwait, the US stock market was up 5%. Lorenz Financial is not recommending any major moves in stock market positioning at this time. If this recommendation changes, we will contact each client with a recommendation.

Quote of the Day

A BusinessWeek magazine cover story in 2006 said, “CEO Jeff Bezos wants to run your business with his web technology. Wall Street wishes he would just mind the store.”

Bezos said in response on May 18, 2022, “I have this old 2006 BusinessWeek magazine cover framed as a reminder. The ‘risky bet’ that Wall Street disliked was AWS (Amazon Web Services – the world’s most versatile and most broadly adopted cloud platform), which generated revenue of more than $62 billion in 2021.” Note, AWS’s revenue was over $128 billion in 2025.

Yes, there are some really smart people on Wall Street, but the smartest people run companies and not just analyze them.

Pop Quiz

Who said the following?

“If you obey the law, you should be protected. But if you break the law, you must pay for your crime.”

Hint: The time was the summer of 1984. It was a presidential election year, and Ronald Reagan was running for his second term. George H. W. Bush was his running mate.

The answer to this month’s Pop Quiz is at the bottom of the newsletter.

The Economy

Employment

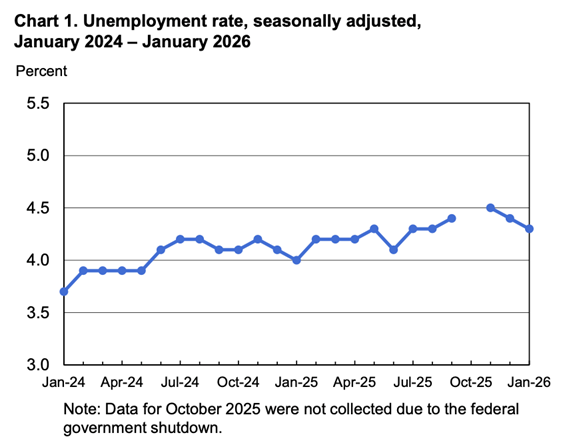

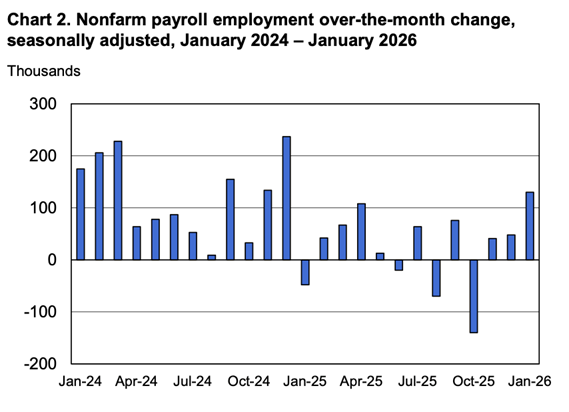

Total U.S. nonfarm payroll employment rose by 130,000 in January. The official unemployment rate, U-3, decreased to 4.3%. The November and December 2025 combined employment numbers were revised lower by 17,000 than previously reported.

Chart 1 below is based on the Bureau of Labor Statistics official unemployment rate, U-3.

Chart 2 below shows the two-year trend of employment growth.

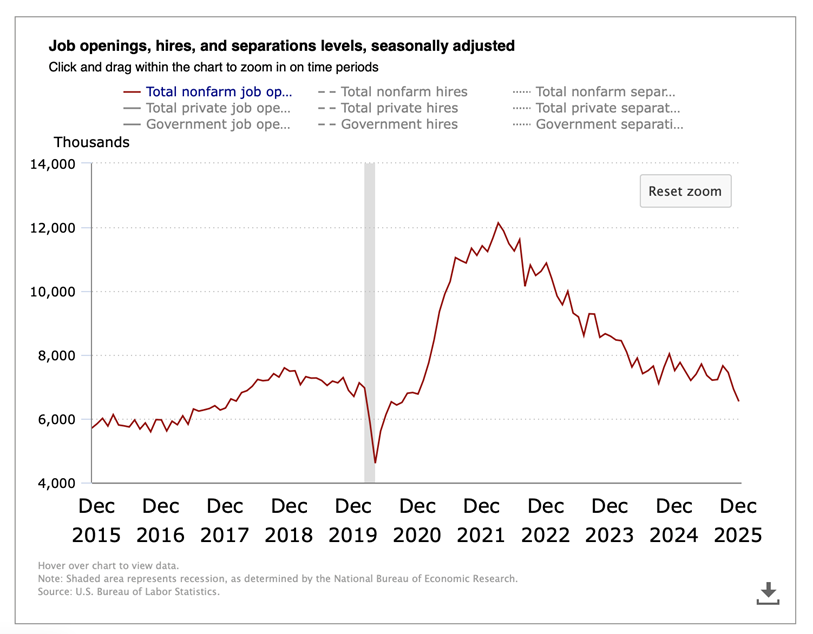

The Job Openings & Labor Turnover Survey (JOLTS) decreased to 6.5 million open jobs across the country as of the last business day in December. It was 7.1 million in November. The 10-year chart below shows that the downward trend continues in open jobs since March 2022.

The seasonally adjusted Total U.S. Unemployment Rate, U-6, decreased to 8.0% in January as compared to 8.4% in November. There were 7.9 million people unemployed in January, aged 16 and older. In December, it was 7.0 million people unemployed.

January Unemployment Rates by Education Level

Average hourly earnings of all employees on private nonfarm payrolls were up 3.7% in January compared to a year ago. It was 3.8% in December.

| Less Than High School Diploma | 5.2% |

| High School Graduate, No College | 4.5% |

| Some College, Associate's Degree, or Skilled Trade Degree | 3.6% |

| Bachelor's Degree or Higher | 2.9% |

Leading Economic Indicators (LEI) sponsored by The Conference Board

The LEI declined 0.2% in December after a revised decrease of 0.3% in November. The Conference Board’s spokesperson said, “The US LEI registered its fifth consecutive monthly decline in December, indicating continued softness in the economy in early 2026. Overall, the LEI signals weaker economic activity at the start of this year.”

Gross Domestic Product (GDP)

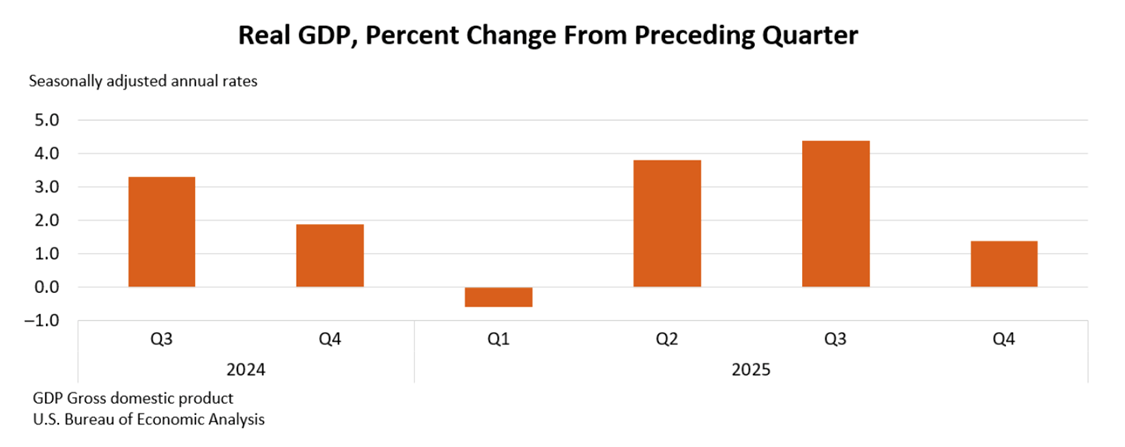

The Bureau of Economic Analysis said the advance estimate for GDP in the fourth quarter of 2025 increased at an annual real rate of 1.4%.

The increase in the fourth quarter GDP reflected an increase in consumer spending and investment. These increases were offset by decreases in government spending and exports. For the year 2024, GDP increased 2.8% and grew 3.2% in 2023.

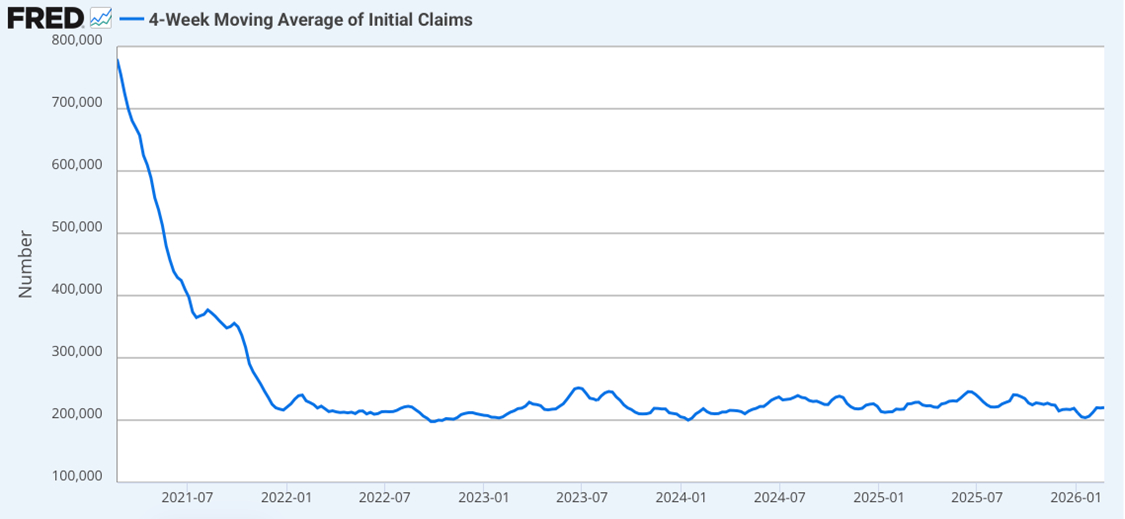

The 4-Week Moving Average of Unemployment Initial Claims is Another Leading Indicator

See the 5-year chart below from the St. Louis Federal Reserve Bank. The higher the graph, the more likely a recession is coming.

The chart is steady-eddy, meaning no recession is in sight! The high number of initial unemployment claims on the left of the chart was the result of the Federal Reserve increasing interest rates seven times in 2022. This resulted in an economic contraction in 2022 and significant labor layoffs that began in mid 2021.

Labor Productivity (quarterly releases only)

Fourth quarter preliminary data will be released on March 5 and revised on March 24.

Annualized and seasonally adjusted, nonfarm labor productivity increased by a whopping 4.9% in the third quarter of 2025 as reported by the Bureau of Labor Statistics. It was originally reported as being 3.3%. So far in 2025, quarterly labor productivity has been:

- 1st qtr -2.1%

- 2nd qtr +4.1%

- 3rd qtr +4.9%

By calendar year, labor productivity grew 2.3% in 2024 and an anemic 1.6% in 2023. High labor productivity is a very good sign for the economy.

Inflation

Annual inflation increased slightly to 2.9% as measured by the Personal Consumption Expenditures (PCE) price index for December. The revised annual November number was 2.8%. The annual core PCE price index, which excludes food and energy, increased slightly in December to 3.0% from 2.8% in November.

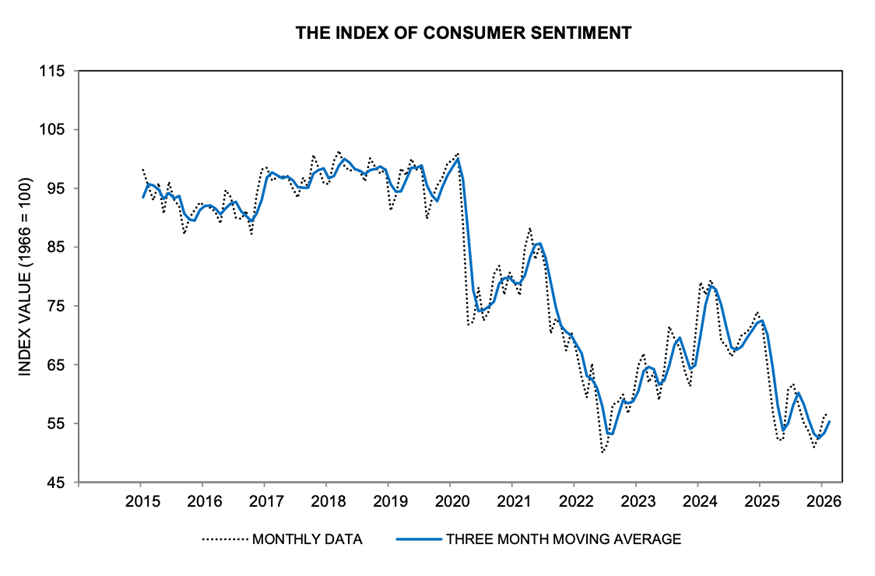

University of Michigan Consumer Sentiment

Consumer sentiment in January increased ever so slightly to 56.6 compared to January’s revised 56.4. See the 10-year chart below.

Overall, consumers do not perceive any material differences in the economy from last month. About 46% of consumers spontaneously mentioned high prices eroding their personal finances; this reading has now exceeded 40% for seven months in a row.

Mortgage Rates and Average Existing Home Prices

As of February 28, 2026, the average 30-year fixed-rate mortgage had an interest rate of 5.99% compared to 6.16% last month. The average 15-year fixed rate mortgage had an interest rate of 5.60%, compared to 5.75% in the previous month.

The median existing single-family home sale price decreased in January 2026 to $396,800, but that was up 0.9% compared to 12 months earlier. The seasonally adjusted annual rate of existing home sales decreased 4.4% compared to a year earlier, according to the National Association of Realtors. The inventory of existing homes for sale increased by 3.4% compared to January 2025. This represents only a 3.7-month supply of homes for sale.

The U.S. National Debt as Issued by the Treasury Department as of February 28, 2026, was:

$38,743,000,000,000.

Last month it was $38,675,000,000,000.

Important Dates in March

THE STOCK MARKET

Commentary

Mohamed El-Erian, speaking on CNBC on February 17, 2026, said, “We are no longer having a love affair with AI like we had last year. The current stock market can be defined by three words:

Volatility – stock prices quickly jumping up and down.

Dispersion – some stock prices doing great, others not so much.

Fragmentation – possible examples:

a) premium hotel stock prices up, medium hotel prices down.

b) oil prices up, natural gas prices down.

c) short-term interest rates down, long-term interest rates up.”

Stephanie Link, on February 26, 2026, said on CNBC, “If you believe in AI, you need data centers. There will be $7 trillion spent to build data centers between now and 2030. This will require a massive upgrade of our electrical grid, as 75% of our grid is over 25 years old! In the same timeframe, the electrical grid update will require $1.4 trillion spent. And then another $1.1 trillion is going to be needed to expand our electrical grid (More power, Scotty!).”

So, there is more opportunity in the stock market than just AI, chips, and technology. We also like the financial, health care, energy, and industrial sectors. Please stay diversified.

Stock Market Valuation

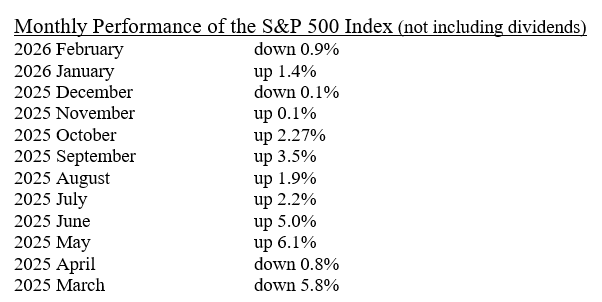

On Feb 26, 2026, Mike Wilson, CIO of Morgan Stanley, said on CNBC, “There are many things going on in the stock market besides AI. We believe we are coming out of a rolling recession from the 4th quarter 2025, where the November stock index was up 0.1% and in December down 0.1%. We believe this rolling correction is now 70 to 80% complete. But we also believe near term volatility is likely to continue for a while longer.”

“Of note is the spread between the top 50 stocks and the bottom 50 stocks, year to date, is 68%. This is the greatest spread we have seen in 20 years.”

“Without a doubt, the economy is strengthening. The 4th quarter GDP number was weak because of the government shutdown. Productivity is running above 4% – that’s great! We are seeing a capital expense boom and not just in data centers.”

“Stocks did great last year in anticipation of the economic boom this year. The stock market is always anticipating – it is an excellent leading indicator of economic activity. I am still very bullish for the second half of 2206. The market will continue to broaden out from technology due to the achievement of higher earnings in most companies.”

The S&P 500 Index closed on February 27, 2026 at 6,878.88. Year to date, the Index, as per the exchange-traded fund, VOO, was up 0.62%. This fund includes dividends.

• Markets are volatile • Always consult your financial advisor before investing

Recent Annual S&P 500 Performance As Per The Exchange Traded Fund, VOO

2025: +17.82%

2024:+24.98%

2023: +26.32%

2022: -18.19%

2021: +28.78%

2020: +18.29%

2019: +31.35%

Recommended Action for Your Stock Portfolio

In alphabetical order, our favorite S&P 500 sectors are:

- Energy

- Financials

- Health Care

- Industrials

- Technology

Our favorite stock market growth fund is GARP. It’s a 5-star, Gold rated fund by Morningstar.

Our favorite stock market blended fund is CGDV. It’s a 5-star, Gold rated fund by Morningstar.

Our favorite stock market value fund is OAKMX. It’s a 4-star Gold rated fund by Morningstar.

∙ Not FDIC Insured ∙ No Bank Guarantee ∙ May Lose Value

Financial Markets Vocabulary

The easy mindset of AI by some companies and investors is “doing the same activities with fewer people.”

But this is not the potential of AI. The real strength of AI is the augmentation of labor, or the enhancement and amplification of the labor force. The achievement of the real advantage of AI will take time, and certainly, some companies, in error, will initiate layoffs.

Over the next few years, we will probably see strong GDP growth, but muted employment growth.

OK, Now What Do I Do?

Mark has had numerous conversations with prospective clients. Some of those conversations go something like this:

Mark asks, “Broadly speaking, how do you want your retirement money to be invested?”

The prospective client responds, “I want my money safe.”

It’s almost impossible to ask the next question without being viewed as a know-it-all, but it is really a serious question. Mark then asks, “Safe from what?”

There are all kinds of risks – even with bank CDs with full FDIC coverage! What risk do they have? The risk with CD’s is that they will not provide the growth or income needed to stay ahead of the negative impacts of inflation and taxes. It’s OK to buy some CD’s, but don’t put anything close to 100% of your money in CD’s. That would be risky.

So, everyone needs to understand there are risks with all types of investing. Put your money in your mattress, and your house burns down. Put your money under a rock, and someone comes along and builds an apartment building. Put your money in real estate, and a very undesirable establishment opens up next door. Put your money overseas, and you have added currency risk. The stock market has plenty of risks. Bonds have two basic risks – interest rate risk and credit risk. Investing is all about understanding your own risk tolerance and then finding the mix of stocks, bonds, cash, and other assets that will provide the growth and income you need without taking unnecessary risks.

That task is challenging, and many people need help to properly allocate their retirement funds. If you need assistance, our recommendation is to work with a fiduciary, a Registered Investment Advisor, to come up with the best allocation for YOU.

• Not insured by any bank or government • Subject to risk & possible loss of principal

Our Financial Bad Boy This Month

This month, our bad boy is “private credit”. Here is some recent analysis.

Boaz Weinstein, founder of the hedge fund Saba Capital, said regarding private credit in late February, “All you need is the snowball to start going down the hill, and the total collapse in private credit will have begun. Blue Owl, an alternative asset manager, is right in the middle of that. I think we are in the super-early innings of the private credit wheels coming off the car.”

Marc Lasry, founder and CEO of Avenue Capital Group, also said in late February, “Of course we should be concerned about the pricing of private credit loans made to non-public software companies. Today would you want to make one of these loans at the same price when the loan was made? NO!”

“Today, due to the advancement of AI, a loan company would want more collateral than six months ago. Anyone today who would want to buy one of these loans would only offer $0.80 on the dollar. A buyer would not buy these loans at PAR, i.e., face value.”

On February 24, Bloomberg reported the following headline: “Private credit fears deepen within UBS, a premier Swiss multinational investment bank, who warns of a 15% default rate of loans within private credit funds.”

Lloyd Blankfein, former CEO of Goldman Sachs, said on private credit, “Why are you (the big brokerage houses) going into this dangerous territory just to make your business a little bit bigger when that represents such a big potential problem in the future? These securities are opaque, sold with high fees, illiquid, and carry high risks.”

“To the extent you are selling these funds to institutions, no one cares. But if you are selling to individuals, who then lose a bunch of money, it’s terrible! I think it is so short-sighted of these brokers to get into private credit for these reasons.”

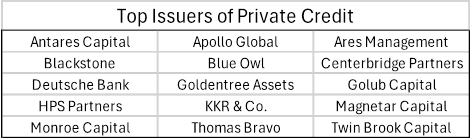

OK, so who are some of the big issuers of private credit funds?

Funds of these companies, or any company that is selling private credit funds, are to be totally avoided!

MAYBE ALL THE MONEY SPENT ON DATA CENTERS IS NOT THAT GREAT

Corporate costs can be measured by “percent of average annual U.S. GDP”. For example, the costs of the Apollo Space program, which sent 24 American astronauts to the moon from 1960 to 1973, were only 0.2% of the average annual U.S. GDP during those years.

So how do the costs of AI data centers compare to other large expenses in America’s history?

PERCENT OF U.S. AVERAGE ANNUAL GDP

- The Louisiana Purchase in 1803: 3.0%

- Projected capital expense for Meta, Amazon, Microsoft, Alphabet in 2026: 2.1%

- U.S. Railroads 1850 to 1859: 2.0%

- U.S. Interstate Highway System 1955 to 1970: 0.4%

- Apollo Space Program 1960 to 1973: 0.2%

So why is the media so frantic about the expenses of the above hyperscaler companies? In our opinion, the media tries to get us all excited about something so we viewers will be sure and “Tune in tomorrow for the latest!” The vast majority of news media is not just about reporting the news anymore, but it’s about manipulating the news so as to increase viewership and ratings, promote the news organization’s agenda, and increase the media company’s profits.

The Bond Market

Commentary

The CNBC guest below being posed questions is Mohamed El-Erian, Chief Economist with Allianz and President of Queens’ College, Cambridge.

Q1: “Do you think the 10-year Treasury at 4% makes sense?”

A1: “I am really scratching my head. We have had strong economic growth. Oil prices have stepped higher. We have foreigners becoming less enthusiastic to buy US Treasuries. Real GDP is at 4%. What I think has happened is investors have become overextended in risk assets (stocks). In the past few weeks, stocks have sold off, and the safe asset, the 10-year US Treasury, has been aggressively bought driving the yield down from 4.5% to 4.0%. From a valuation and fundamental perspective, it is very hard to justify a 4.0% 10-year Treasury. The yield is too low.”

Q2: “What is your target for the second half of 2026?”

A2: I think we will see the yields go back towards 4.5%. I think we are in a range from 4.0% to 4.5% with the future average yield being closer to 4.5% than 4.0%.”

Recommended Action for Your Safest Money

Our investor’s safest money recommendations are now listed below and in order with the top line, PRPFX, representing the potentially highest returns, is reasonably credit safe, but likely will have the highest volatility. This month we are adding short-term US corporate high yield (junk bond) funds as an option for PART of a family’s safe money.

- Permanent Portfolio mutual fund, PRPFX, gold bullion, or silver bullion.

- Short-term U.S. corporate high-yield, junk bond funds.

- Short-term U.S. investment-grade corporate or securitized bond funds.

- FDIC bank or NCUA credit union, 1 to 4 yr CDs, paying at least 3.7%.

- Bank or brokerage-house, high-yield savings or money market accounts, 3.7% min.

- US Treasury Bills of 1 year, or Treasury Notes of 2, 3 or 4 years.

- U.S. Savings I-Bonds which have a max contribution of $10,000 per account per year, are tax deferred for 30 years, do not drop in value like bonds drop in value when interest rates rise, interest is paid and compounded monthly, and the interest rate resets every six months based on inflation (the higher the inflation, the higher the interest rate).

The bottom option in the list above, U.S. Savings I-Bonds, is the most credit safe and has the lowest volatility but potentially the lowest returns. We recommend everyone spread their “safe money” over at least five of the seven ideas above.

Due to the low return of all these investment products, investors should not put 100% or anything close to that in these products. These products are only for an investor’s safest money or perhaps 5% to 40% of an investor’s total portfolio. These products are credit safe, but they will not provide the growth or income needed to stay ahead of, or even keep up with, taxes plus inflation.

Past performance is not a guarantee of future results.

Pop Quiz Answer

Who said the following? “If you obey the law, you should be protected. But if you break the law, you must pay for your crime.”

Answer:

Well, surprise! The speaker was Geraldine Ferraro, the democratic vice-presidential candidate running with Walter Mondale. The occasion was Ms. Ferraro’s acceptance speech at the Democratic National Convention in San Francisco.

Today, some Democrats advocate for “cashless bail”, meaning people indicted for misdemeanors and some nonviolent felony charges can be released from jail prior to their trial, with no means to guarantee they will show up for their trial. Other progressive policies that, at a minimum, appear to contribute to increased crime include “defund the police”, downgrading of felonies to misdemeanors, prosecutors who decline to prosecute certain crimes, and a general tolerance for social disorder (remember Portland, Oregon, summer of 2020).

This has been a massive change in attitude towards crime within the democratic party. For those who wish to bring a revolution to America, step one is to bring chaos to the people.