Welcome to the November 2025 Newsletter. This month, we’re discussing the economy, employment, financial terminology, and more.

Summary

The current feeling across many economists is, if we were getting all the government data on inflation, employment, and GDP, the numbers would confirm the economy has a little higher inflation than previously. Many companies are not hiring as expected, but economic growth is significantly above 3% which is very good. The Fed cut interest rates another 0.25% in late October which will help to stimulate the economy. The Fed’s move is saying it’s more important right now to be fighting unemployment with lower interest rates rather than fighting higher inflation with elevated interest rates.

The S&P 500 Index has had a great run, with the previous six consecutive months moving up. That is relatively rare, so we should expect a down month or two in the near term.

Repeating what we said last month: everyone should use their patience and courage to maintain their stock positions. Yes, as the decades roll by, we all tend to get a little more conservative in our investments. Therefore, it’s OK to downsize the percentage we have in the stock market occasionally. Make sure your portfolio is low-cost, highly diversified, and taxable accounts are tax-efficient. Everyone’s portfolio should match the investor’s risk tolerance, which means staying away from alternative investments. Beware of being too conservative and having all of one’s money in bank CDs etc. Our list towards the bottom of this newsletter shows options for your safe money. But this list is not the place for the majority of your money, as the returns are too low to even keep up with inflation plus (future) taxes. Even the most conservative investors should have 35% to 40% of their assets in the stock market or other growth strategies.

Quote of the Day

On October 14, 2025, Jamie Dimon, CEO of JPMorgan Chase, said during his company’s 3rd quarter earnings call, “I probably shouldn’t say this, but when you see one cockroach, there are probably more.”

Dimon was referring to the asset category of “private credit” and the significant risks associated with that investment category no matter what the promoters of private credit say. These risks become much more visible when some borrowers begin to declare bankruptcy. See the section below titled, “OK, Now What Do I Do?”.

Pop Quiz

What is the purpose of the Federal Open Market Committee (FOMC) and how many meetings do they have per year?

The answer to this month’s Pop Quiz is at the bottom of the newsletter.

The Economy

Employment

There has been no update to this category due to the government shutdown. Total U.S. nonfarm payroll employment rose by a paltry 22,000 in August. The official unemployment rate, U-3, increased slightly to 4.3%. The June and July 2025 combined employment numbers were revised lower by 21,000 than previously reported.

Chart 1 below is based on the Bureau of Labor Statistics official unemployment rate, U-3.

Chart 2 below shows the two-year trend of employment growth.

The Job Openings & Labor Turnover Survey (JOLTS) decreased slightly to 7.2 million open jobs across the country as of the last business day in July. It was 7.4 million in the prior month. The 10-year chart below shows that the downward trend continues in open jobs since March 2022.

The seasonally adjusted Total U.S. Unemployment Rate, U-6, increased slightly to 8.1% in August as compared to 7.9% in the prior month. There were 7.7 million people unemployed in August, aged 16 and older. Last month, it was 7.8 million people unemployed.

September Unemployment Rates by Education Level

Average hourly earnings of all employees on private nonfarm payrolls were up 3.7% in August compared to a year ago. It was 3.9% the previous month.

| Less Than High School Diploma | 6.7% |

| High School Graduate, No College | 4.3% |

| Some College, Associate's Degree, or Skilled Trade Degree | 3.2% |

| Bachelor's Degree or Higher | 2.7% |

Leading Economic Indicators (LEI) sponsored by The Conference Board—No Update

The LEI declined by 0.5% in August after a revised increase of 0.1% in July. The Conference Board’s spokesperson said, “Besides persistently weak manufacturing new orders and consumer expectations, labor market developments also weighed on the Index with an increase in unemployment claims. Overall, the LEI suggests economic activity will continue to slow.”

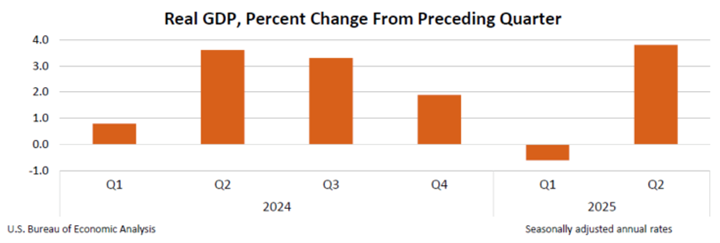

Gross Domestic Product (GDP)

The Bureau of Economic Analysis said the final estimate for GDP in the second quarter of 2025 increased at a significant annual real rate of 3.8%! This economy is ripping! GDP for the first quarter of 2025 was revised to a minus 0.6%.

The increase in the second quarter GDP reflected a decrease in imports, which is a subtraction in the GDP calculation, and an increase in consumer spending. For the year 2024, GDP increased 2.8% and grew 3.2% in 2023.

Labor Productivity – No Update

Annualized and seasonally adjusted, nonfarm labor productivity increased by 3.3% in the second quarter of 2025 as reported by the Bureau of Labor Statistics. It was originally reported as being 2.4%. For the same quarter a year ago, labor productivity increased 1.5%.

By calendar year, labor productivity grew a revised 2.8% in 2024 and 1.9% in 2023. High labor productivity is a good sign for the economy.

Inflation — No Update

Annual inflation increased slightly to 2.7% as measured by the Personal Consumption Expenditures (PCE) price index for August. The revised annual July number was 2.6% during the prior 12 months. The annual core PCE price index, which excludes food and energy, was unchanged in August at 2.9%.

University of Michigan Consumer Sentiment

Consumer sentiment in October declined to 53.6 compared to September’s revised 55.1. See the 10-year chart below.

Overall, consumers perceive few material changes in economic circumstances from last month; inflation and high prices remain at the forefront of consumers’ minds. Year ahead inflation expectations ebbed to 4.6% this month from 4.7% last month.

Mortgage Rates and Average Existing Home Prices

As of October 31, 2025, the average 30-year fixed-rate mortgage had an interest rate of 6.28%, compared to 6.37% last month. The average 15-year fixed rate mortgage had an interest rate of 5.81%, compared to 5.89% last month.

The median existing single-family home sale price decreased month over month in September 2025 to $420,700, but that was up 2.3% from 12 months earlier. The seasonally adjusted annual rate of existing home sales increased 4.5% compared to a year earlier, according to the National Association of Realtors. The inventory of existing homes for sale increased by 1.3% compared to August. This represents a 4.6-month supply of homes for sale.

The U.S. Public Debt as Issued by the Treasury Department as of October 31, 2025, was:

$38,055,000,000,000. Note, $38 trillion is 1,000 times greater than $38 billion.

Last month it was $37,546,000,000,000.

Important Dates in November

THE STOCK MARKET

Commentary

JPMorgan announced on October 13, 2025, a new $1.5 trillion, decade-long initiative called its Security and Resiliency Initiative. The money, of which $10 billion is JPMorgan’s own money, is to be invested as follows:

- Defense and Aerospace (ITA)

- Frontier Technologies including artificial intelligence, blockchain, robotics, autonomous driving, and 3D printing (ARKQ, BOTZ, ROBT)

- Energy Technologies (VDE for broad energy exposure, VPU for broad utility exposure, ICLN for the volatile clean energy sector, and VOLT for the volatile nuclear power sector).

ETFs as listed above in “( )” cover the sectors within JPMorgan’s announcement. The volatility of some of these ETFs is very high. Investing in these ETFs contains substantial risk!

On a less volatile topic, here are six companies currently paying a high dividend.

Remember, don’t put all your eggs in one basket! If you are interested in these stocks, don’t put more than 4% of your stock market money into any one stock.

Stock Market Valuation

Ed Yardeni of Yardeni Research has raised his 2025 end of year S&P 500 estimate from 6,800 to 7,000.

The S&P 500 Index closed on October 31, 2025 at 6,840.20. Year to date the Index including dividends is up 17.47%.

Recent Annual S&P 500 Performance As Per The Exchange Traded Fund, VOO

2024: +24.98%

2023: +26.32%

2022: -18.19%

2021: +28.78%

2020: +18.29%

2019: +31.35%

Recommended Action for Your Stock Portfolio

Technology stocks seem to be the highest performing stocks since October 2022, but not all tech companies are in a bull market. So, where to invest today in technology? Here are some of our ideas.

Companies are either exploring or using artificial intelligence (AI). AI requires tremendous amounts of data, and then there are results and conclusions to keep track of. Where will all this happen? In the cloud. Who are the dominant players in the cloud? Alphabet, Amazon, IBM, Microsoft, Meta, Oracle, and Salesforce. Try the ETF, QQQ.

All lists in this category are in alphabetical order.

If a company is putting all this data on the cloud, they have to protect it. Which companies dominate cybersecurity? Cisco Systems, CrowdStrike, CyberArk Software, Fortinet, Microsoft, Palo Alto Networks, and Zscaler. Try the ETF, BUG.

All of this computing requires microchips. Who dominates semiconductor design?

AMD, Broadcom, Micron, Nvidia, and Qualcomm. Try the ETF, SMH.

Who dominates chip manufacturing? Intel, Micron, and Taiwan Semiconductor. Try the ETF, SMH.

Who dominates the chip equipment manufacturers? ASML, Applied Materials, KLA Corp, and Lam Research. Try the ETF, SMH.

Another sector has been a recent disappointment – the housing sector. One of these days, companies that make housing will take off as the US is short at least 5 million homes. A well-represented exchange-traded fund for the housing sector is the exchange traded fund, ITB.

A speculative sector is air taxis. Two companies stand out. ACHR and JOBY. These are companies that are not yet making a profit, and their stock prices are highly volatile, so invest here with caution!

∙ Not FDIC Insured ∙ No Bank Guarantee ∙ May Lose Value

Financial Markets Vocabulary

As defined benefit retirement plans have all but disappeared, a new crop of retirement plans has emerged. Here is a basic rundown. Typically, an employee will have a choice of one of the plans below from their employer in addition to Social Security.

Defined Contribution Plans

401K - An employer-sponsored retirement plan offered by large and small companies. The plans receive contributions from employees and employers. Employee contributions can be before income taxes are withheld (a Traditional plan) or after income taxes are withheld (a Roth plan). Contribution can be invested into a limited list of stock, bond, and cash funds as selected by the employer. After retirement, the proceeds can be rolled over to an IRA.

403B - Retirement plans offered by non-profit organizations and public educational institutions. They function similarly to a 401K.

457 – Retirement plans offered by state and local governments. The Indiana retirement plan, for example, is called the Public Employee Retirement Fund (PERF). It also functions like a 401K.

The federal government offers its Thrift Savings Plan (TSP) to employees hired after December 31, 1983. For employees hired before January 1, 1984, it is called the Civil Service Retirement System (CSRS).

Dave Ramsey recommends that every family contribute 15% of the family’s gross income (before taxes) for their retirement.

OK, Now What Do I Do?

Perhaps this month we will be beating a dead horse, but we continue to strongly believe alternative investments are no place to put one’s money due to the high level of hidden risks. Specifically, let’s look at the private credit market, which is one category of “alternative investments”. This is what Jamie Dimon was talking about during JPMorgan’s third quarterly conference call when Dimon said, “When you see one cockroach, there are probably more.”

Dimon was referring to the very recent bankruptcy of First Brands, an auto-parts supplier. The marketplace lost confidence in their use of off-balance sheet debt – a big no-no. Then Tricolor, a chain of auto dealers, declared bankruptcy following the company being accused of pledging fictitious car loans as collateral.

And now a third example of the disaster potential of private credit is below in our “Bad Boy” article.

Our conclusion is, alternative investment categories such as private credit, private equity, non-traded REITS, and Crypto, etc., have no place for an investor’s money. The stock market has enough risks without doubling down with speculation.

∙ Not Insured by Any Bank or Governement ∙ Subject to Risk & Possible Loss of Principal

Our Financial Bad Boy This Month

BlackRock is Stung By Alleged Fraud

The Wall Street Journal, October 31, 2025, page B1

BlackRock’s private credit investing arm and other lenders are trying to recover hundreds of millions of dollars after falling victim to what they called a “breathtaking” fraud, marking another breakdown in an opaque corner of the U.S. private debt markets. BlackRock is the world’s largest asset manager – larger than Vanguard, Schwab or J.P. Morgan.

Note to our readers: Here we go again with another example of why everyone should avoid the “private debt” market and everything labeled “alternative investments”!

Back to the article – the fraud victims, like BlackRock, have accused Bankim Brahmbhatt, the owner of the telecom services company, Broadband Telecom and Bridgevoice, of fabricating accounts receivable that were supposed to be used as loan collateral.

Lawyers for the victims wrote, “Brahmbhatt created an elaborate balance sheet of assets that existed only on paper.” The lawyers also allege Brahmbhatt transferred assets, that should have been pledged as collateral, to offshore accounts in India and Mauritius. Brahmbhatt and his companies all declared bankruptcy on August 12.

Brahmbhatt disputes the allegations of fraud, his lawyer said.

The Bond Market

Commentary

Following the Federal Open Market Committee (FOMC) meeting of October 28 and 29, Chair Powell said at his press conference, “Although some important federal government data has been delayed due to the shutdown, the data that remains suggest the outlook for employment and inflation has not changed significantly since our previous meeting. Today, the FOMC decided to lower our policy interest rate by ¼ percentage point. We also decided to conclude the reduction to our securities holding on December 1.”

The vote was not unanimous as one voting member wanted a ½ point cut and another member wanted no interest rate cut at all.

Recommended Action for Your Safest Money

Our recommendations for an investor’s safest money have not changed from last month. Our recommendations, in no particular order, are:

Our recommendations, in no particular order, are:

- Short-term U.S. Investment-Grade Corporate or Securitized bond funds.

- FDIC bank or NCUA credit union CDs paying at least 4%.

- US Treasury Bills of 1 year, or Treasury Notes of 2, 3 or 4 years.

- Bank & brokerage-house, high-yield savings & money market accounts (4% min.).

- Permanent Portfolio mutual fund, PRPFX.

- U.S. Savings I-Bonds which have a max contribution of $10,000 per account per year, are tax deferred for 30 years, do not drop in value like bonds drop in value when interest rates rise, interest is paid and compounded monthly, and the interest rate varies every six months based on inflation (the higher the inflation, the higher the interest rate).

There are six ideas above for an investor’s safe money. We recommend everyone spread their safe money over at least four of these ideas.

Due to the relatively low return of these investment products, investors should not put 100% or anything close to that in these products. These products are only for an investor’s safest money or perhaps 5% to 30% of an investor’s total portfolio. These products are credit safe, but they will not provide the growth or income needed to stay ahead of, or even keep up with, taxes and inflation.

Past performance is not a guarantee of future results.

Pop Quiz Answer

What is the purpose of the Federal Open Market Committee (FOMC) and how many meetings do they have per year?

Answer:

The FOMC is part of the Federal Reserve. The FOMC sets the nation’s monetary policy in order to achieve maximum employment and price stability. The committee meets eight times a year, typically in Washington, DC, and once a year in Jackson Hole, Wyoming. (Members of the FOMC lead a tough life!)

The 19 members of the FOMC consist of seven Governors based in Washington, DC, one of whom is the committee Chair, and 12 Presidents, with one president from each of the 12 regional Federal Reserve Banks. The Governors vote during every meeting, but only half of the Presidents get to vote each year, rotating every other year.

In local news, the former St. Louis Federal Reserve Bank President, James Bullard, is now the Dean of the Mitch Daniels School of Business at Purdue University in West Lafayette. This was formerly known as the Krannert School of Management. Mr. Bullard was quite the catch for Purdue.