Welcome to the October 2025 Newsletter. This month, we’re discussing the economy, employment, financial terminology, and more.

Summary

The economy has been zooming along in the second quarter of 2025. Inflation is not yet at 2% (the Fed’s target), but it’s not out of control either. The labor market is starting to see a few cracks and that is why the Fed lowered short-term interest rates by 0.25% at their September meeting. Likely they will initiate at least one more cut later this year. The Fed’s move is saying it’s more important right now to be fighting unemployment with lower interest rates rather than fighting inflation with higher rates.

The stock market has had a fantastic run. See the 3-year chart below of the S&P 500 Index from October 1, 2022 to September 30, 2025.

We could take a breather, meaning a slight stock market downturn, at any time. But Lorenz Financial believes there is so much cash sitting in money market funds (last reported to be $7.7 trillion), as soon as the market drops 3 to 6%, money will rush in and buy up stocks.

Everyone should use their patience and courage to maintain their stock positions. Yes, as the decades roll by, we all tend to get a little more conservative in our investments. Therefore, it’s OK to reduce the percentage we have in the stock market occasionally. Make sure your portfolio is low cost; highly diversified and taxable accounts must be tax efficient. Everyone’s portfolio should match their risk tolerance. Beware of being too conservative and having mostly all of one’s money saved in bank CDs etc. Our list towards the bottom of this newsletter shows options for your safe money. But this list is not the place for the majority of your money as the returns are too low to even keep up with inflation plus (future) taxes. Even the most conservative investors should have 35% to 40% of their assets in the stock market.

Quote of the Day

From July to October 1940 the German Luftwaffe fought Britain’s Royal Air Force (RAF) for air superiority over London, the whole of Great Britian, and the English Channel.

It was the first military campaign fought entirely by air forces. The RAF was limited primarily due to their low number of trained fighter pilots, but those they had fought with overwhelming confidence and bravery. By the end of October Hitler had given up, and the British survived to fight another day.

In paying tribute to the heroism and sacrifice of the RAF pilots during the battle, Winston Churchill said in a speech to the House of Commons, “Never in the field of human conflict was so much owed by so many to so few.”

Pop Quiz

Which Home Depot department had the greatest dollar sales in 2024?

The answer to this month’s Pop Quiz is at the bottom of the newsletter.

The Economy

Employment

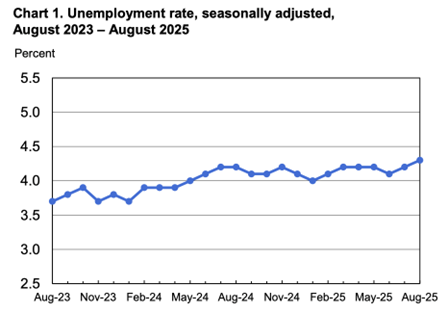

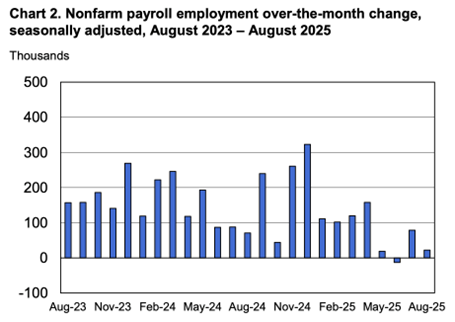

Total U.S. nonfarm payroll employment rose by a paltry 22,000 in August. The official unemployment rate, U-3, increased slightly to 4.3%. The June and July 2025 combined employment numbers were revised lower by 21,000 than previously reported.

Chart 1 below is based on the Bureau of Labor Statistics official unemployment rate, U-3.

Chart 2 below shows the two-year trend of employment growth.

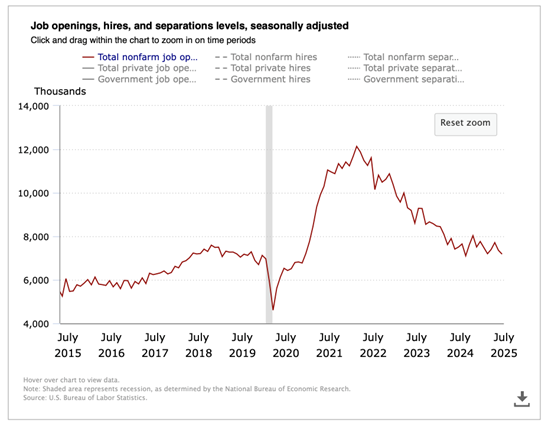

The Job Openings & Labor Turnover Survey (JOLTS) decreased slightly to 7.2 million open jobs across the country as of the last business day in July. It was 7.4 million in the prior month. The 10-year chart below shows the downward trend continues in open jobs since March 2022.

The seasonally adjusted Total U.S. Unemployment Rate, U-6, increased slightly to 8.1% in August as compared to 7.9% in the prior month. There were 7.7 million people unemployed in August, age 16 and older. Last month it was 7.8 million people unemployed.

August Unemployment Rates by Education Level

Average hourly earnings of all employees on private nonfarm payrolls were up 3.7% in August compared to a year ago. It was 3.9% the previous month.

| Less Than High School Diploma | 6.7% |

| High School Graduate, No College | 4.3% |

| Some College, Associate's Degree, or Skilled Trade Degree | 3.2% |

| Bachelor's Degree or Higher | 2.7% |

Leading Economic Indicators (LEI) sponsored by The Conference Board

The LEI declined by 0.5% in August after a revised increase of 0.1% in July. The Conference Board’s spokesperson said, “Besides persistently weak manufacturing new orders and consumer expectations, labor market developments also weighed on the Index with an increase in unemployment claims. Overall, the LEI suggest economic activity will continue to slow.”

Gross Domestic Product (GDP)

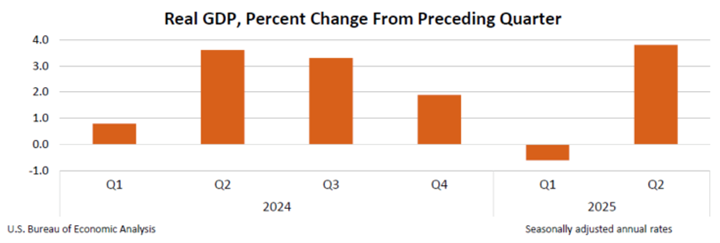

The Bureau of Economic Analysis said the final estimate for GDP in the second quarter of 2025 increased at a significant annual real rate of 3.8%! This economy is ripping! GDP for the first quarter of 2025 was revised to a minus 0.6%.

The increase in the second quarter’s GDP reflected a decrease in imports, which is a subtraction in the GDP calculation, and an increase in consumer spending. For the year 2024, GDP increased 2.8% and grew 3.2% in 2023.

Labor Productivity – Second Quarter Data, Revised September 4

Annualized and seasonally adjusted, nonfarm, labor productivity increased by 3.3% in the second quarter of 2025 as reported by the Bureau of Labor Statistics. It was originally reported as being 2.4%. For the same quarter a year ago, labor productivity increased 1.5%.

By calendar year, labor productivity grew a revised 2.8% in 2024 and 1.9% in 2023. High labor productivity is a good sign for the economy.

Inflation

Annual inflation increased slightly to 2.7% as measured by the Personal Consumption Expenditures (PCE) price index for August. The revised annual July number was 2.6% during the prior 12-months. The annual core PCE price index, which excludes food and energy, was unchanged in August at 2.9%.

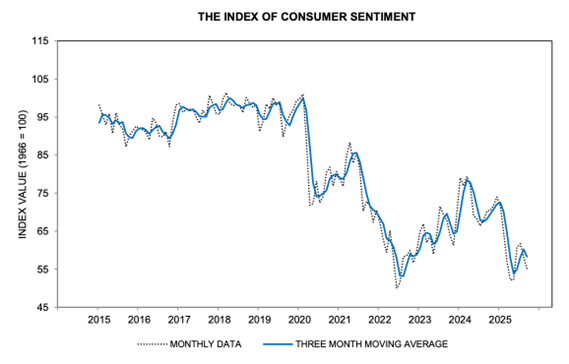

University of Michigan Consumer Sentiment

Consumer sentiment in September declined to 55.1 compared to August’s revised 58.2. See the 10-year chart below.

Consumer sentiment eased by about 5% from last month but remains above the low readings seen in April and May of this year. Consumers continue to express frustration over the persistence of high prices. Consumer interviews this month highlighted the fact that they feel pressure from both the prospect of higher inflation as well as the risk of weaker labor markets.

Mortgage Rates and Average Existing Home Prices

As of September 30, 2025, the average 30-year fixed-rate mortgage had an interest rate of 6.37%, compared to 6.50% last month. The average 15-year fixed rate mortgage had an interest rate of 5.89%, compared to 5.86% last month.

The median existing single-family home sale price increased in August 2025 to $427,800, up 1.9% from 12 months earlier. The volume of existing home sales decreased 0.3% compared to a year earlier according to the National Association of Realtors. The inventory of existing homes for sale decreased by 1.3% compared to July. This represents a 4.6-month supply of homes for sale. The desired supply-target is 6 months.

The U.S. Public Debt as Issued by the Treasury Department as of September 30, 2025, was:

$37,546,000,000,000.

Last month it was $37,292,000,000,000

Important Dates in October

THE STOCK MARKET

Commentary

First, we have David Tepper, President and Founder of Appaloosa Management, the most successful hedge fund ever. Tepper said on CNBC the week of September 15, “I don’t love the multiples of today but how do I not own the market? I’m not ever going to be fighting the Fed, especially, when the market is telling me two or three more interest rate cuts are coming.”

Second, Stephanie Link, Chief Investment Strategist at Hightower Advisors, said on CNBC on September 22, “The market is expensive, but the Fed is cutting interest rates into a strong economy, we are going to see double digit earnings growth, free cash flow growth in expected to be 14% year over year, companies are buying back a ton of their own stock, and companies are seeing margin expansion.”

JPMorgan assembled the following information on how much some companies are buying back their own stock. The bank said, “S&P 500 companies have announced buybacks at an unprecedented rate, with close to $960 billion committed so far this year. This significantly surpasses the three-year average of $644 billion.

Some Companies Who Have Announced Stock Buybacks

-

Tapestry — $3 billion

-

Charles Schwab — $20 billion

-

Airbnb — $6 billion

-

Bank of America — $40 billion

-

Uber — $20 billion

-

Southwest — $2 billion

-

Newmont — $3 billion

-

Novartis — $10 billion

-

Morgan Stanley — $20 billion

-

JPMorgan — $50 billion

Stock Market Valuation

Below we have two comments from Goldman Sachs managers from September 22, 2025, on CNBC.

First is Tony Pasquariello, Global Head of Hedge Fund Coverage. He said, “Do I love the current positioning setup and the tactical risk/reward ratio? I don’t.”

“With that said, do I think an investor should be stepping in front of the US mega cap tech freight train? I don’t.” Here Tony’s phrase, ‘stepping in front’ means to ‘buy now’. Therefore, he is saying, this is not the time to buy the US mega cap tech stocks, also known as the magnificent seven, because they have risen so much the past three years.

Pasquariello continues with, “But this is a bull market (an up market), and the primary trend is higher.”

Pasquariello ended with some statistics saying, “Since the start of 2009, the Nasdaq 100 has been up 16 of 17 years (assuming this year remains positive). The cumulative return of these 100 stocks has been over 2,200%.”

“Breaking down the returns, we find this is where the returns came from

75% came from corporate earnings.

16% came from dividends.

9% came from expansion of the price/earnings ratio.”

But even in a bull market, the market does not go straight up. For example, Nvidia (NVDA) just had four down weeks in a row. In the big picture, this is a sarcastic, “Big Whoop!”, meaning for long-term investors who are using their courage and patience, we don’t care about a four-week blip.

Also, we have David Kostin, Goldman Sachs’ Chief Equity Strategist. Kostin raised his 12-month S&P 500 target to 7,200.

Ed Yardeni of Yardeni Research has raised his 2025 end of year S&P 500 estimate from 6,600 to 6,800. He also said the S&P 500 could reach 7,000 yet this year.

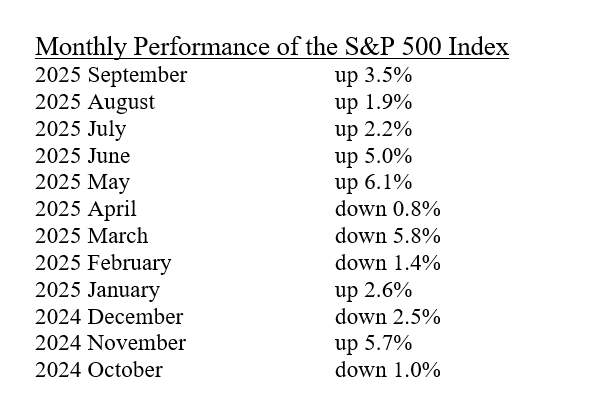

The S&P 500 Index closed on September 30, 2025 at 6,688.46. Year to date the Index is up 13.7%.

Recent Annual S&P 500 Performance As Per The Exchange Traded Fund, VOO

2024: +24.98%

2023: +26.32%

2022: -18.19%

2021: +28.78%

2020: +18.29%

2019: +31.35%

Recommended Action for Your Stock Portfolio

Below in the section titled, Recommended Action for Your Safest Money, we have added a new investment option for your safest money – the mutual fund, Permanent Portfolio. Its symbol is PRPFX.

As of mid-September 2025, this fund is made up of:

-

30% US stocks

-

3% International stocks

-

16% US and Switzerland government bonds

-

21% A-rated and BBB-rated investment-grade US corporate bonds

-

20% Gold bullion

-

4% Silver bullion

-

6% Cash, including US dollars and Swiss francs

This diversified no-load fund has an expense ratio of 0.81% per year and a minimum investment of $1,000. Over the past 15 years, this fund has had an average annual return of 7.4%. How is its return compared to its volatility? The answer to that question is to examine the fund’s Sharpe Ratio. Over the past three years, the fund has an excellent Sharpe Ratio of 1.35. Lorenz Financial likes funds with a Sharpe Ratio over 1.

This is not a high growth fund. This is not a pure stock fund; this is a highly diversified, moderately allocated, mutual fund suitable for part of an investor’s safe money.

∙ Not FDIC Insured ∙ No Bank Guarantee ∙ May Lose Value

Financial Markets Vocabulary

This month we are offering comments from Lloyd Blankfein, former Goldman Sachs CEO, on the topic of “Federal Reserve independence”.

Question: What do you think about the Fed independence issue?

Answer: “You know we (the federal government) are a big borrower. If we were a corporate borrower, we would want the Chief Financial Officer (CFO) of the company to be reassuring to its lenders by indicating, “I am going to protect the value of my company so I can be in a position to pay you back and not default”.

“If you are the U.S. borrower and you are borrowing in dollars, you can always print more dollars so you will always be able to pay back your borrowed dollars. So, can the U.S. government default? It can in effect, default by inflating the currency so the dollars that are paid back are worth a lot less than when borrowed.”

“Well, if the government evolves to a position where it looks like it is going to inflate the currency, that is like telegraphing to the stock and bond markets that the government is much more likely to default than what the borrowers previously thought. Then as a lender I will choose to either not loan the government any additional money or I will charge the government a higher interest rate.”

“That’s why as the Fed lowers short-term rates as we expect, the hope that long-term rates will follow them lower, might be a false hope.”

“So, I think this ‘Fed independence’, protecting our currency, maintaining the integrity of the Federal Reserve, and that the government will pay investors back dollars that are as valuable as the dollars loaned, is extremely key! And anyone who undermines this is reaping a significant disadvantage without any corollary to an advantage.”

OK, Now What Do I Do?

This month, lets discuss, long-term stock market net returns – meaning returns after inflation, spending in retirement, and saving for retirement.

First let’s look at stock market returns. The S&P 500 is up 13.7% so far in 2025, before subtracting inflation. Over the past decade, the S&P 500 has returned an average of 15% annually, far in excess of its long-term annualized returns of 10.3%, again before subtracting inflation. The obvious worry is that stocks have become extraordinarily expensive. The more subtle concern is that a booming stock market breeds complacency!

To understand long-term stock market average annual returns, we need to analyze the numbers on an “after-inflation basis” because a dollar in 1800 was very different than a dollar in 2025 BECAUSE OF INFLATION. Author Ed McQuarrie did so going back to January 1793. He looked at every 30-year rolling period from then until present day. For example, the first 30-year period was January 1793 to December 1822. The second 30-year period was February 1793 to January 1823, and so on for over 2,400 different 30-year rolling periods.

What is so magical about a 30-year period? Well for many people, they are going to end up working and saving for retirement over 30 years and then be in retirement 30 years. It is a reasonable way to look at the data.

The average annual stock market return after inflation since 1793 has been 6.1%. 160 of those three-decade periods had an average stock market return after inflation of 3%. Another 302 of those periods had returns less than 4%.

Over the three decades ended in December 2023, US stock returned an annualized 6.9% after inflation. However, over the 360 months ended in July 1982, they earned only 4.7% and in the 30 years ended May 1932, stocks gained only 0.9% annually after inflation.

So, whether you are 25 or 65 years old, we cannot count on stock market returns of 15% a year to dramatically grow our retirement savings!

Second, let’s look at perhaps the worst retirement advice that is out there. That is, “Well you will only spend 80% in retirement compared to what you are spending before retirement.” That is nonsense according to researchers Ed McQuarrie and Bill Bernstein. Several studies have shown that on average, people spend 93% to 97% as much in retirement as they did when they were still working.

So how does all of this tell an investor how much to save? Let’s be a little conservative and say a portfolio of stock, bonds, and cash will earn 5% after inflation. Therefore, to maintain family spending at the same rate during 30 years of retirement as they did before retirement, the family would need to save 12% of their gross (not net) income for the prior 30 years.

Want to be a little more conservative and assume only a 4% average annual return after inflation for 30 year? Then start saving 15% of pre-tax income. And if hard times are in front of us and only a 3% return can be expected, well then savings will need to be 21% of gross income. Dave Ramsey recommends families save 15% of the family’s gross income each year for retirement.

Let’s say you want to be extra careful and expect only a 3% return after inflation in the stock market, and you plan to work 40 years and only spend 20 years in retirement. How much do you have to save each year? 10% per year. There is no getting around we must save, save, save for retirement, and we must start early!

To counteract the consequences of miserable long-term returns, an investor has only three choices: Save more, work longer or take more risk. Saving more is by far the easiest and certainly the safest path.

∙ Not insured by any bank or government ∙ Subject to risk & possible loss of principal

Our Financial Bad Boy This Month

Financier Charged

The Wall Street Journal, September 9, 2025, page B10

Federal prosecutors have charged Paul Regan (no relation to Donald T. Regan, President Reagan’s Chief of Staff 1985 to 1987) with securities and wire fraud. The U.S. attorney’s office in Manhattan alleged that Regan defrauded more than 300 investors of at least $50 million based on materially false and misleading documents given to potential clients.

Investors were “guaranteed” annual rates of return of 10.5% to 15%. Then instead of investing client’s money, the assets were used for Regan’s personal expenses and to pay prior investors with the new money coming in – a Ponzi scheme!

Regan failed to disclose to investors that he had been barred for life from the securities industry in 2004. He also failed to disclose he was fined by a state securities regulator for allegedly forging documents and stealing $140,000 from an elderly customer with dementia.

More recent clients were Richard and Kimberly Whitacre of Maryland. They invested virtually all of Richard Whitacre’s $763,000 retirement account with the notorious, Mr. Regan. What a great idea! Investors should put all their eggs in one basket!

Last known to be living in the South American country of Colombia, Regan couldn’t be reached for comment.

The Bond Market

Commentary

Following the Federal Open Market Committee (FOMC) meeting of September 16 and 17, Chair Powell said at his press conference, “My colleagues and I remain squarely focused on achieving our dual mandate goals of maximum employment and stable prices. Today the FOMC decided to lower our policy interest rate by ¼ percentage point. We also decided to continue to lower our securities held on the Fed’s balance sheet.”

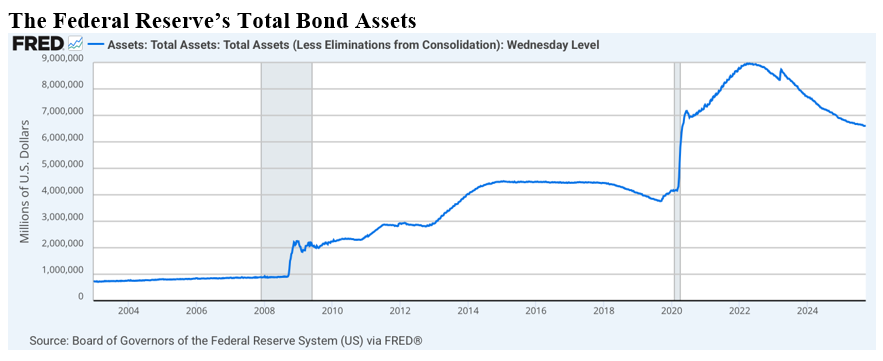

The chart below shows the Federal Reserve’s total assets on its balance sheet from 2004 to present. The content of the balance sheet’s assets is primarily US Treasury notes and bonds. The intent of growing the balance sheet in 2008 and 2020 was to lower long-term interest rates by first reducing the supply of long-term Treasuries available to Treasury buyers. The lower the supply of Treasuries increased the price of these long-term Treasuries. As the price of long-term Treasuries went up, their yield went down – which was the intent. The lower the supply, the lower the long-term interest rates as long as demand remained constant. This tactic was successful.

Chair Powell continued saying, “Recent indicators suggest the growth of economic activity has moderated. GDP rose at a pace of around 1.5% in the first half of the year, down from 2.5% last year. The moderation in growth largely reflects a slowdown in consumer spending. In contrast, business investment in equipment and intangibles has picked up from last year’s pace. But activity in the housing sector remains weak.”

“In the labor market, the unemployment rate edged up to 4.3% in August but remains little changed over the past year at a relatively low level. Labor demand has softened, and the recent pace of job creation appears to be running below the breakeven rate needed to help the unemployment rate remain constant.”

“Inflation has eased significantly from its highs in mid-2022 but remains somewhat elevated relative to our 2% goal. The overall personal consumption expenditures (PCE) inflation gauge rose 2.7% over the 12 months ending in August while core PCE, which excludes food and energy, rose 2.9%.”

“In the near term, risks to inflation are tilted to the upside and risks to employment to the downside – a challenging situation. Accordingly, we judged it appropriate at this meeting to take another step towards a more neutral interest rate stance.”

Recommended Action for Your Safest Money

Our recommendations for an investor’s safest money have changed slightly from last month. Our recommendations, in no particular order, are:

Our recommendations, in no particular order, are:

- Short-term U.S. Investment-Grade Corporate or Securitized bond funds.

- FDIC bank or NCUA credit union CDs paying at least 4%.

- US Treasury Bills of 1 year, or Treasury Notes of 2, 3 or 4 years.

- Bank & brokerage-house, high-yield savings & money market accounts (4% min.).

- Permanent Portfolio mutual fund, PRPFX.

- U.S. Savings I-Bonds which have a max contribution of $10,000 per account per year, are tax deferred for 30 years, do not drop in value like bonds drop in value when interest rates rise, interest is paid and compounded monthly, and the interest rate varies every six months based on inflation (the higher the inflation, the higher the interest rate).

There are six ideas above for an investor’s safe money. We recommend everyone spread their safe money over at least four of these ideas.

Due to the relatively low return of these investment products, investors should not put 100% or anything close to that in these products. These products are only for an investor’s safest money or perhaps 5% to 30% of an investor’s total portfolio. These products are credit safe, but they will not provide the growth or income needed to stay ahead of, or even keep up with, taxes and inflation.

Past performance is not a guarantee of future results.

Pop Quiz Answer

Which Home Depot department had the greatest dollar sales in 2024?

Answer:

The Garden department, by far and away.

-

Garden — $20.8 billion

-

Appliances — $14.1 billion

-

Power — $13.1 billion

-

Building Materials — $12.4 billion

-

Plumbing — $12.4 billion

-

Lumber — $11.8 billion

-

Hardware — $9.0 billion