Welcome to the December 2025 Newsletter. This month, we’re discussing the economy, employment, financial terminology, and more.

Summary

On November 28, Stephanie Link, Chief Investment Strategist and Portfolio Manager at Hightower Advisors, said on CNBC, “In December the stock market is typically up 1.5% on average. So far, the economy continues to surprise to the upside. We had a very good weekly Jobless Claims this week. The Jobless Claims numbers are cooling (going a little higher) but not collapsing. Durable goods orders rose almost 10%. This past month the Producer Price Index (PPI) inflation numbers were pretty tame but still elevated at 2.7%. This is better than what we have been seeing over the last few years. So, add it all up and the GDP is running at 3.5% to 4% - and its above trend. This is leading to double digit corporate earnings expectations for next year. I do believe we are going to see an absolute broadening out of the stock market.”

Quote of the Day

Arthur C. Brooks, Harvard Business School Professor, said on November 2 on the David Rubenstein Show, “The reason the United States is such a great and successful country is because people have personal aspirations for something better for their own life and their children’s lives.”

Brooks went on to say, “Teaching my first semester at Harvard, I created a class called 'Leadership and Happiness'. On the first day of class I tell the students, 'You think if you obtain money, power and pleasure, these things will get you happiness for free. But that is a lie. The right solution is for you to search for happiness and then you will have the success you truly crave.'”

It was no accident that Thomas Jefferson wrote in the Declaration of Independence, “We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable rights, that among them are life, liberty, and the pursuit of happiness.”

Pop Quiz

One of the basic concepts of American capitalism allows for “individual resourcefulness and creativity to upset and overrun the establishment”. Business professors call this “creative destruction”. What are some examples of “creative destruction”?

The answer to this month’s Pop Quiz is at the bottom of the newsletter.

The Economy

Employment

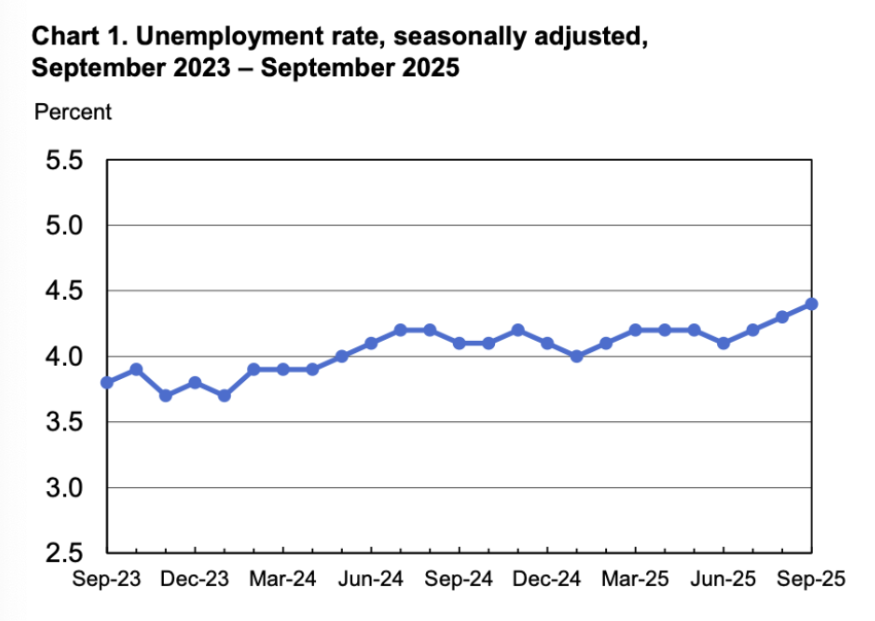

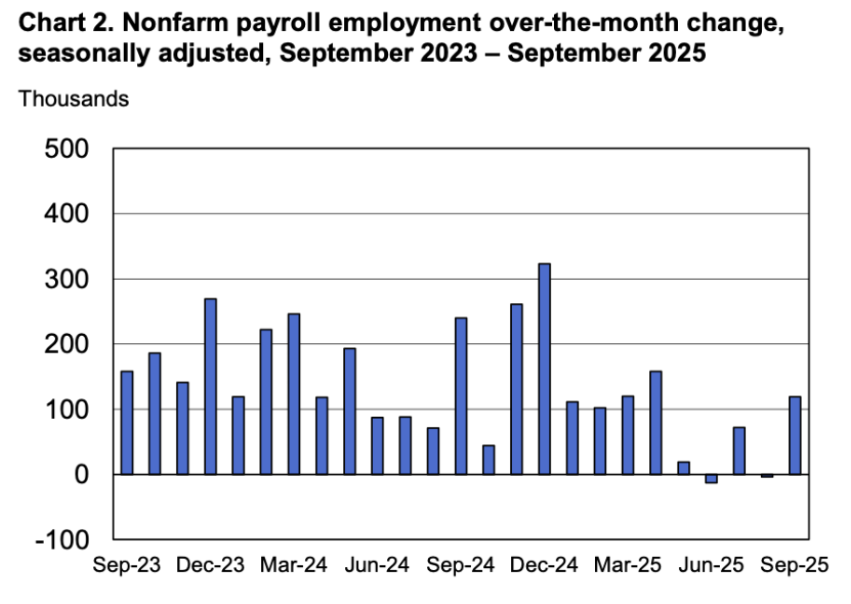

Total U.S. nonfarm payroll employment rose by a surprising 119,000 in September. The official unemployment rate, U-3, increased slightly to 4.4%. The July and August 2025 combined employment numbers were revised lower by 33,000 than previously reported.

Chart 1 below is based on the Bureau of Labor Statistics official unemployment rate, U-3.

Chart 2 below shows the two-year trend of employment growth.

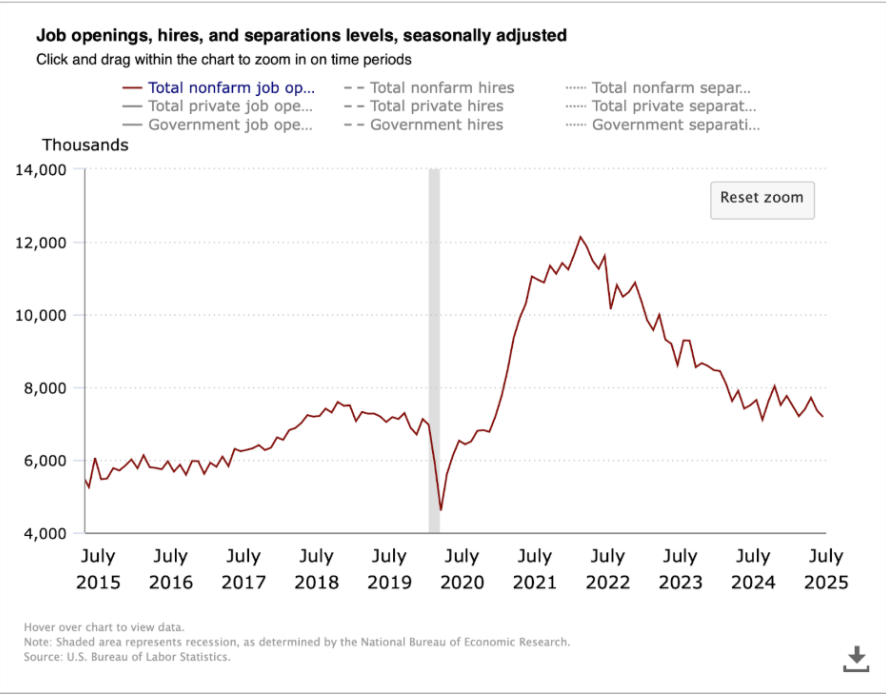

The Job Openings & Labor Turnover Survey (JOLTS) decreased slightly to 7.2 million open jobs across the country as of the last business day in July. It was 7.4 million in the prior month. The 10-year chart below shows that the downward trend continues in open jobs since March 2022.

The seasonally adjusted Total U.S. Unemployment Rate, U-6, decreased slightly to 8.0% in September as compared to 8.1% in the prior month. There were 7.3 million people unemployed in September, aged 16 and older. Last month, 7.7 million people were unemployed.

September Unemployment Rates by Education Level

Average hourly earnings of all employees on private nonfarm payrolls were up 3.8% in September compared to a year ago. It was 3.7% the previous month.

| Less Than High School Diploma | 6.8% |

| High School Graduate, No College | 4.2% |

| Some College, Associate's Degree, or Skilled Trade Degree | 3.4% |

| Bachelor's Degree or Higher | 2.8% |

Leading Economic Indicators (LEI) sponsored by The Conference Board—No Update

The LEI declined by 0.5% in August after a revised increase of 0.1% in July. The Conference Board’s spokesperson said, “Besides persistently weak manufacturing new orders and consumer expectations, labor market developments also weighed on the Index with an increase in unemployment claims. Overall, the LEI suggest economic activity will continue to slow.”

Gross Domestic Product (GDP) – No update below. Hoping for an update at end of December.

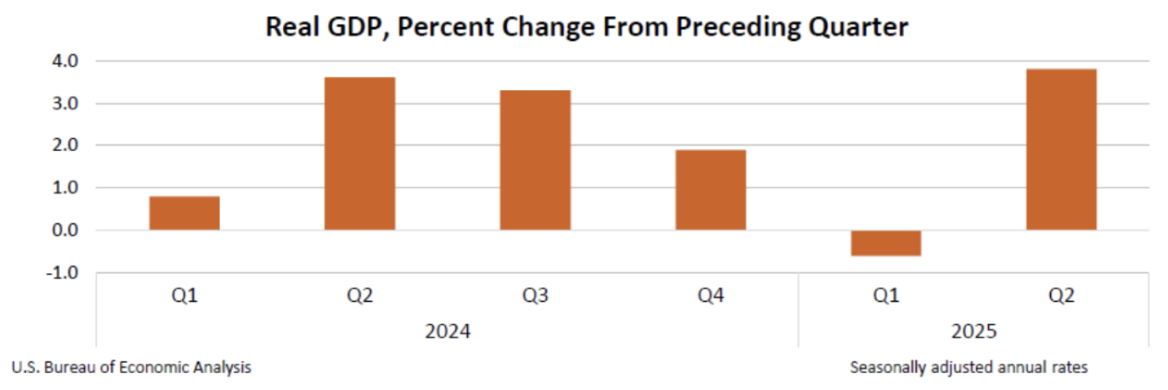

The Bureau of Economic Analysis said the final estimate for GDP in the second quarter of 2025 increased at a significant annual real rate of 3.8%! This economy is ripping! GDP for the first quarter 2025 was revised to a minus 0.6%.

The increase in the second quarter GDP reflected a decrease in imports, which is a subtraction in the GDP calculation, and an increase in consumer spending. For the year 2024, GDP increased 2.8% and grew 3.2% in 2023.

Labor Productivity – No Update

Annualized and seasonally adjusted, nonfarm, labor productivity increased by 3.3% in the second quarter of 2025 as reported by the Bureau of Labor Statistics. It was originally reported as being 2.4%. For the same quarter a year ago, labor productivity increased 1.5%.

By calendar year, labor productivity grew a revised 2.8% in 2024 and 1.9% in 2023. High labor productivity is a good sign for the economy.

Inflation – No update below. Expect new info on December 5, 2025

Annual inflation increased slightly to 2.7% as measured by the Personal Consumption Expenditures (PCE) price index for August. The revised annual July number was 2.6% during the prior 12 months. The annual core PCE price index, which excludes food and energy, was unchanged in August at 2.9%.

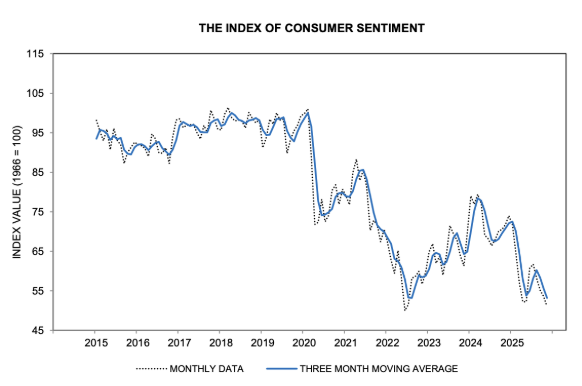

University of Michigan Consumer Sentiment

Consumer sentiment in November declined to 51.0 compared to October’s revised 53.6. See the 10-year chart below.

Consumers remain frustrated about the persistence of high prices and weakening incomes. Year ahead inflation expectations ebbed to 4.5% this month from 4.6% last month.

Mortgage Rates and Average Existing Home Prices

As of November 30, 2025, the average 30-year fixed-rate mortgage had an interest rate of 6.33%, compared to 6.28% last month. The average 15-year fixed rate mortgage had an interest rate of 5.66%, compared to 5.81% last month.

The median existing single-family home sale price remained steady month over month in October 2025 to $420,600, but that was up 2.2% from 12 months earlier. The seasonally adjusted annual rate of existing home sales increased 1.7% compared to a year earlier, according to the National Association of Realtors. The inventory of existing homes for sale increased by 10.9% compared to October 2024. This represents a 4.4-month supply of homes for sale.

The U.S. Public Debt as Issued by the Treasury Department as of November 30, 2025, was:

$38,349,000,000,000. Note, $38 trillion is 1,000 times higher than $38 billion.

Last month it was $38,055,000,000,000.

Important Dates in December

THE STOCK MARKET

Commentary

Howard Marks, Co-Chairman of Oaktree Capital Management, has now published 160 memos (as he calls them) over the past 35 years. Most everyone on Wall Street eagerly waits for each one.

Marks said recently on CNBC, “In the first memo of October 1990, I wrote about performance. I had just met with a client in Minneapolis who explained he had been running a pension fund for 14 years. His stock portfolio had never been above the 27th percentile and never lower than the 47th percentile during those 14 years.”

“So where did he end up overall? One might think the 37th percentile. No, this money manager for those 14 years was in the top 4%. Why, because he never shot himself in the foot by taking excessive risk at the wrong time. He was unlike his peers who blew up their portfolio at least once during those 14 years.”

Even though the above comment is about controlling risk, we cannot go overboard and put all our money in bank CDs. Every investor needs to find the balance that is best for them between volatility and safety on one hand and reasonable long-term performance on the other.

Stock Market Valuation

Ed Yardeni of Yardeni Research has continued his support for 2025 end-of-year S&P 500 target of 7,000. Yardeni is also predicting 2026 year-end will achieve 7,700 based on record corporate profits, broadening market participation, and an economy that refuses to falter.

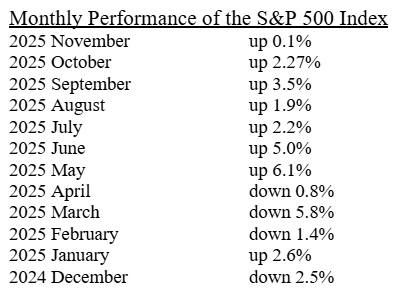

The S&P 500 Index closed on November 30, 2025 at 6,849.09. Year to date, the Index including dividends is up 17.8%.

Recent Annual S&P 500 Performance As Per The Exchange Traded Fund, VOO

2024: +24.98%

2023: +26.32%

2022: -18.19%

2021: +28.78%

2020: +18.29%

2019: +31.35%

Recommended Action for Your Stock Portfolio

Yes, a lot of speculators have made money by buying crypto, but at Lorenz Financial, we strongly recommend staying away from it. Why?

Crypto is not a “storehouse of value”. A storehouse of value should retain its purchasing power, be portable, and reasonably liquid over a long period of time. We believe crypto is too volatile to be a good storehouse of value.

Crypto is not a currency. To be spendable, an asset needs to be divisible, legal tender, and accepted by businesses in exchange for the business’s products or services. Crypto, as defined by the IRS, is not a currency.

But to an investment speculator, crypto does not need to be a storehouse of value or currency. They just need it to have positive price momentum. But lately, crypto does not even have that.

What does crypto have? Well, it does not have any assets or even a promise behind it. The only thing it has is hope. Such as, “I HOPE there is a guy out there who will pay me more tomorrow for my crypto than what I paid yesterday.” The only group that really likes crypto is kidnappers and extortionists.

Our recommendation: if you have no crypto, don’t buy any. If you have crypto, sell it.

∙ Not FDIC Insured ∙ No Bank Guarantee ∙ May Lose Value

Financial Markets Vocabulary

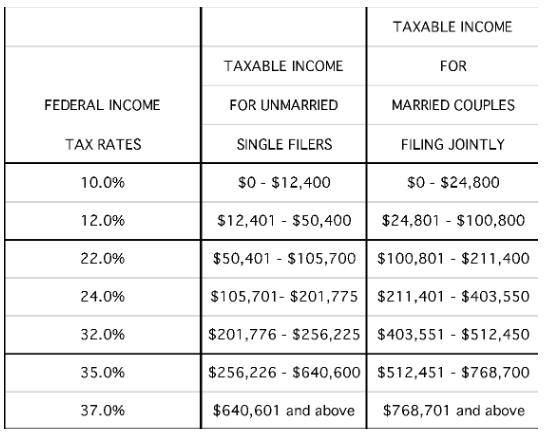

FEDERAL INCOME TAX BRACKETS FOR 2026

The standard deduction in 2026 for single filers increases to $16,100 from $15,750 in 2025. For married couples, the standard deduction will be $32,200, up from $31,500.

UPDATING OUR FOLDING MONEY

America’s folding money, i.e. our paper currency, will receive the latest anti-counterfeiting features in the following years:

2026: $10

2028: $50

2030: $20

2032: $5

2034: $100

Today’s $100 bill already has many of the latest anti-counterfeiting features, so it is last on this list.

OK, Now What Do I Do?

Beware of Costly Mistakes When Naming Beneficiaries

Almost all of our financial accounts now require naming beneficiaries. When signing a will, we tend to pay attention to its contents. But, for example, when starting work with a new company, how much time did you spend thinking about filling out the beneficiary form?

OK, which accounts require a beneficiary?

- Retirement Accounts: 401 (k), 403b, 457, Federal Government Thrift Saving Plan, State retirement plans such as Indiana’s PERF.

- IRAs: Traditional, Roth, SEP, Simple, Spousal, Custodial, Self-Directed, and Rollovers.

- Life Insurance and Annuities

- 529 College Savings Plans

- Health Savings Accounts

- Banks: Payable on Death forms for pretty much any type of bank account.

- Brokerage Accounts: Transfer on Death

Some states even allow Transfer on Death for automobiles and real estate. Indiana is one such state.

It is very important to note that a beneficiary form overrides whatever might be stated in a will. Significant life events can cause the need to review all beneficiary forms. For example, if a beneficiary has died before the account owner, once the account owner has died, if a deceased person is a beneficiary, then the whole estate can be thrown into probate court. Many problems with beneficiary forms can easily be solved while the account owner is alive, but it’s impossible to fix though once the owner has died.

What are some of the issues that develop when a beneficiary form contains an error?

1. Don’t name your estate as the heir; always designate a person or a trust.

2. If, for some reason, a defined beneficiary does not want to receive the proceeds from the deceased, then if secondary beneficiaries are named, they will receive the estate. Therefore, always name secondary beneficiaries.

3. When an account is transferred, always fill out a new beneficiary form. This can occur when a brokerage account is transferred from TRPrice to Vanguard, or vice versa, or an annuity moves from one insurance company to another. This is important as beneficiary forms are not part of the “transfer process”.

4. Under federal law, spouses must be the heirs of a 401K plan unless the spouse has signed a form waiving this right. For example, a husband and wife have 3 children. Then the wife dies, and the man remarries. When he dies, the new wife gets all the 401K – nothing will go to the children, unless the waiver has been signed by the second wife. Please be careful with 401K’s!

5. A family is trying to be careful with their estate. They hire a lawyer to set up a trust. But they forget to change the beneficiary form on the IRAs to now name the trust.

Lorenz Financial always recommends hiring an estate planning attorney in your state to make sure your wishes are converted into the proper paperwork.

∙ Not insured by any bank or government ∙ Subject to risk & possible loss of principal

Our Financial Bad Boy This Month

A Pension Fund’s Mistake is a Lesson for All of Us

Robert Auwaerter is the Vice Mayor of Indian River Shores, Florida. As a former Bond Fund Manager, Auwaerter has been advising the Board of Trustees at the pension plan for the town’s public safety workers and firefighters. The pension fund has about $21 million in total assets. Nearly all of the pension plan’s assets are in publicly traded stocks and bonds – that’s good. But 4% is invested in the U.S. Real Estate Investment Fund, a non-traded portfolio of commercial real estate. This fund is managed by Intercontinental Real Estate, an investment firm in Boston.

This fund is an example of an “alternative investment” that invests not in publicly traded stocks or bonds, but in assets that generally don’t have daily prices. The advocates of private funds say they can provide superior returns to public markets. That’s absolutely true, but there’s a big difference between “can” and “usually do”.

Over the five years ended December 31, 2024, the Intercontinental fund generated an average total return of 0.7% annually. Over the same period, Vanguard’s Real-Estate Index Fund was up an average of 3% annually. Auwaerter says the trustees of the pension plan are reconsidering whether they should invest in real estate at all.

Intercontinental charges 1.1% in annual expenses. That is more than eight times higher than Vanguard’s Real-Estate Index Fund!

Many alternative investments take seven to 12 years or more to pay off, if they do. In the meantime, if you want – or need – to get some or all your money out, you may well be stuck.

The typical alternative fund is “a roach motel”, says Auwaerter. “You come in, and then you can only get out when they liquidate an asset. And you don’t know what that price is going to be down the road, but the range is probably so wide you could drive a Mack truck through it.”

Auwaerter said, “When I bought illiquid stuff, I was getting a return premium for it! Here, it’s a trifecta of bad things: lower returns, higher fees, and no liquidity!”

This is just another example of why we advocate individual investors to stay away from alternative investments.

The Bond Market

Commentary

This month, we are quoting Glenn August, founder and CEO of Oak Hill Advisors in New York City. Mr. August said on CNBC, “To really have distress in the stock and bond markets, you first need a lot of leverage (borrowing), then a recession, and finally forced sellers. Today I do not see a recession anytime soon. The markets have evolved such that there are not forced sellers in the markets and there is not that much leverage in the system.”

Recommended Action for Your Safest Money

Our investor’s safest money recommendations are now listed in order with the top line representing potentially highest returns, credit safe, but highest volatility.

Our recommendations, in no particular order, are:

- Permanent Portfolio mutual fund, PRPFX.

- Short-term U.S. investment-grade corporate or securitized bond funds.

- FDIC bank or NCUA credit union CDs paying at least 3.7%.

- Bank or brokerage-house, high-yield savings or money market accounts (3.7% min.).

- US Treasury Bills of 1 year, or Treasury Notes of 2, 3 or 4 years.

- U.S. Savings I-Bonds which have a max contribution of $10,000 per account per year, are tax deferred for 30 years, do not drop in value like bonds drop in value when interest rates rise, interest is paid and compounded monthly, and the interest rate varies every six months based on inflation (the higher the inflation, the higher the interest rate).

The safe money options at the bottom of the above list are the most credit safe, have the lowest volatility, but potentially the lowest returns. We recommend everyone spread their safe money over at least four of these six ideas.

Due to the relatively low return of these investment products, investors should not put 100% or anything close to that in these products. These products are only for an investor’s safest money or perhaps 5% to 30% of an investor’s total portfolio. These products are credit safe, but they will not provide the growth or income needed to stay ahead of, or even keep up with, taxes and inflation.

Past performance is not a guarantee of future results.

Pop Quiz Answer

One of the basic concepts of American capitalism allows for “individual resourcefulness and creativity to upset and overrun the establishment”. Business professors call this “creative destruction”. What are some examples of “creative destruction”?

Answer:

- The automobile replaced the horse.

- Passenger airplanes replaced passenger trains.

- Smartphones mostly replaced landlines, alarm clocks, and cameras.

- Digital photography replaced film.

- Uber and Lyft are replacing taxis.

- Personal computers and printers replaced typewriters.

- Search websites and especially Wikipedia have replaced encyclopedias.